What Credit Score Do You Need to Rent an Apartment?

It’s the first thing renters worry about — and the answer is more flexible than the rumor mill suggests. Here’s what landlords actually look for.

If you’re about to apply for an apartment, you’ve probably wondered whether your credit score is “good enough.” It’s a fair worry — but the idea of a single magic number is mostly a myth.

There’s no universal credit-score cutoff to rent, and plenty of people with middling or thin credit get approved every day. Here’s how landlords really decide, and what to do if your score isn’t where you’d like.

Is there a minimum credit score to rent?

No single number is required by law or industry, and standards vary widely by landlord, property, and market. A big professionally managed complex may run an automated check with a set cutoff; an individual landlord may not pull credit at all, or may weigh your whole application instead. The same score can be a yes in one building and a no in another.

So rather than chasing a target number, it helps to understand the ranges landlords tend to think in — and the other factors that often matter more.

The ranges landlords tend to look for

As a loose guide, many landlords feel comfortable around the mid-600s and up, competitive big-city markets can lean higher, and more flexible landlords work with scores well below that — especially with a strong overall application. Treat these as soft tendencies, not rules:

- 700+ — rarely a credit obstacle anywhere.

- ~620–700 — fine for most landlords; tight markets may ask for more.

- Below ~620 — approval depends more on income, history, and how you present the rest of your application.

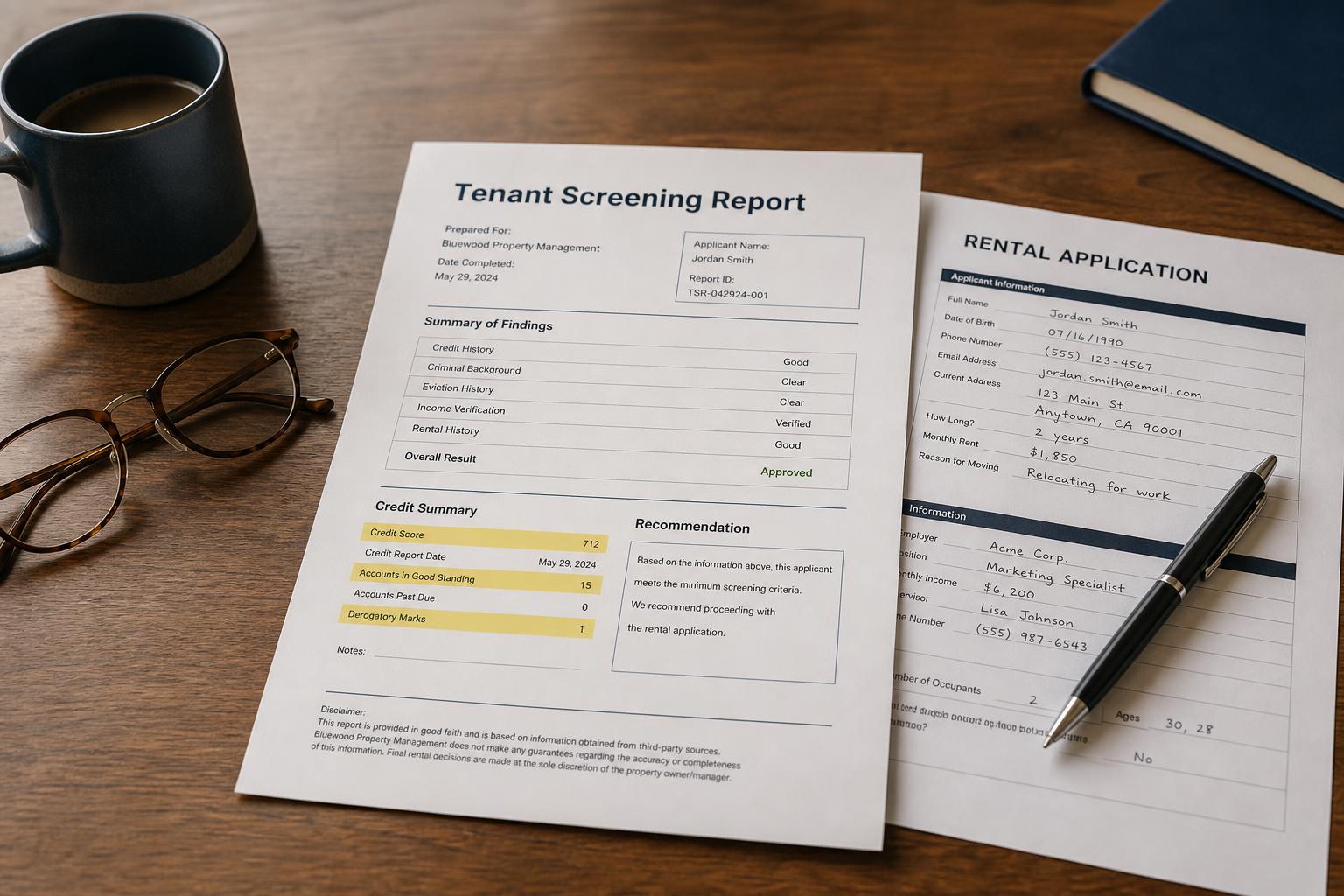

Even these vary, because landlords often look at a tenant-screening report rather than a raw FICO score — here’s how to read your tenant screening report.

Why income and history matter as much as the score

A credit score is only one input. Landlords are really asking, “Will this person pay rent, in full and on time?” They answer it with several things:

- Income — many use a rough rule that rent should be around a third of gross income.

- Rental history — on-time payments and good references from past landlords.

- Employment stability — steady work or proof of reliable income.

- What’s on the report — a prior eviction or a pile of collections can outweigh a so-so score.

A strong showing on these can carry an average score a long way.

What a low score doesn’t doom

A below-average score is a hurdle, not a wall. Renters clear it all the time by giving the landlord other reasons to feel confident: a larger security deposit, a cosigner or guarantor, several months’ proof of income, glowing references, or a short, honest letter of explanation for a past rough patch. None of that changes your score, but all of it changes the decision.

Renting with bad or no credit

If your credit is damaged or simply thin, you have specific playbooks. With no credit history, lean on income, references, and a guarantor. With damaged credit, look for individual landlords and second-chance properties that read the full picture. Two guides go deep on this: second chance apartments and renting with bad credit and no cosigner.

Check your report before you apply

Application fees add up, and every denial can cost you a fee and an inquiry. Before you apply, pull your own credit and tenant-screening reports so you know exactly what a landlord will see — and can correct any errors or prepare an explanation first. A free 15-minute rental credit review walks through what’s likely showing and what may be worth addressing.

Key takeaways

- There’s no universal minimum credit score to rent — standards vary by landlord and market.

- Many landlords lean toward the mid-600s+, but flexible ones work with lower scores.

- Income, rental history, and references often matter as much as the score itself.

- A larger deposit, a cosigner, proof of income, or a letter of explanation can offset a low score.

- Check your own credit and tenant-screening reports before you apply, so there are no surprises.

See what a landlord will see — before you apply

A free 15-minute review walks through what’s on your credit report and what may be worth addressing or explaining, so you apply where you actually stand a chance.

Free · about 15 minutes · no credit card · no obligation.

Sources: Consumer Financial Protection Bureau (CFPB) — tenant-screening reports and your rights as a renter; Fair Credit Reporting Act (FCRA) — adverse action and your right to the report used. Landlord criteria vary by property, market, and state; this is general education, not legal advice.