Know what landlords see

How to Read Your Tenant Screening Report — and Spot Mistakes

The report a landlord pulls can decide your application before you ever meet. Here’s how to get your own copy, read every section, and catch the errors that quietly cause denials.

Quick answer

A tenant screening report bundles your rental history, credit, public records, and sometimes eviction and background data — compiled by consumer reporting agencies regulated by the Fair Credit Reporting Act (FCRA). Landlords use it to decide your application, often with an automated score.

You have the right to see your own report, and the FCRA gives you a free copy after any denial based on it. Reading it before you apply — and disputing anything inaccurate — is one of the most useful things you can do.

What is a tenant screening report?

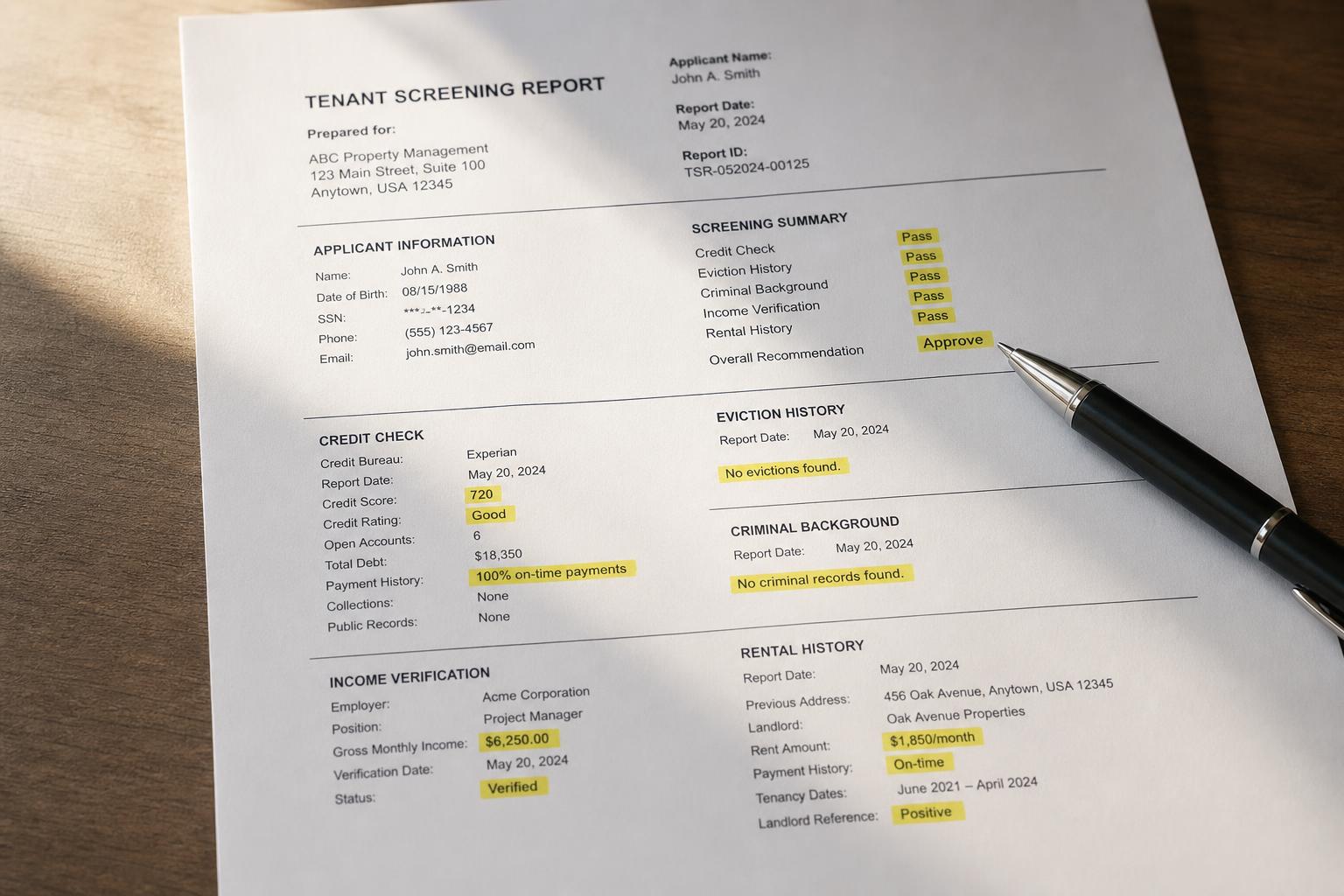

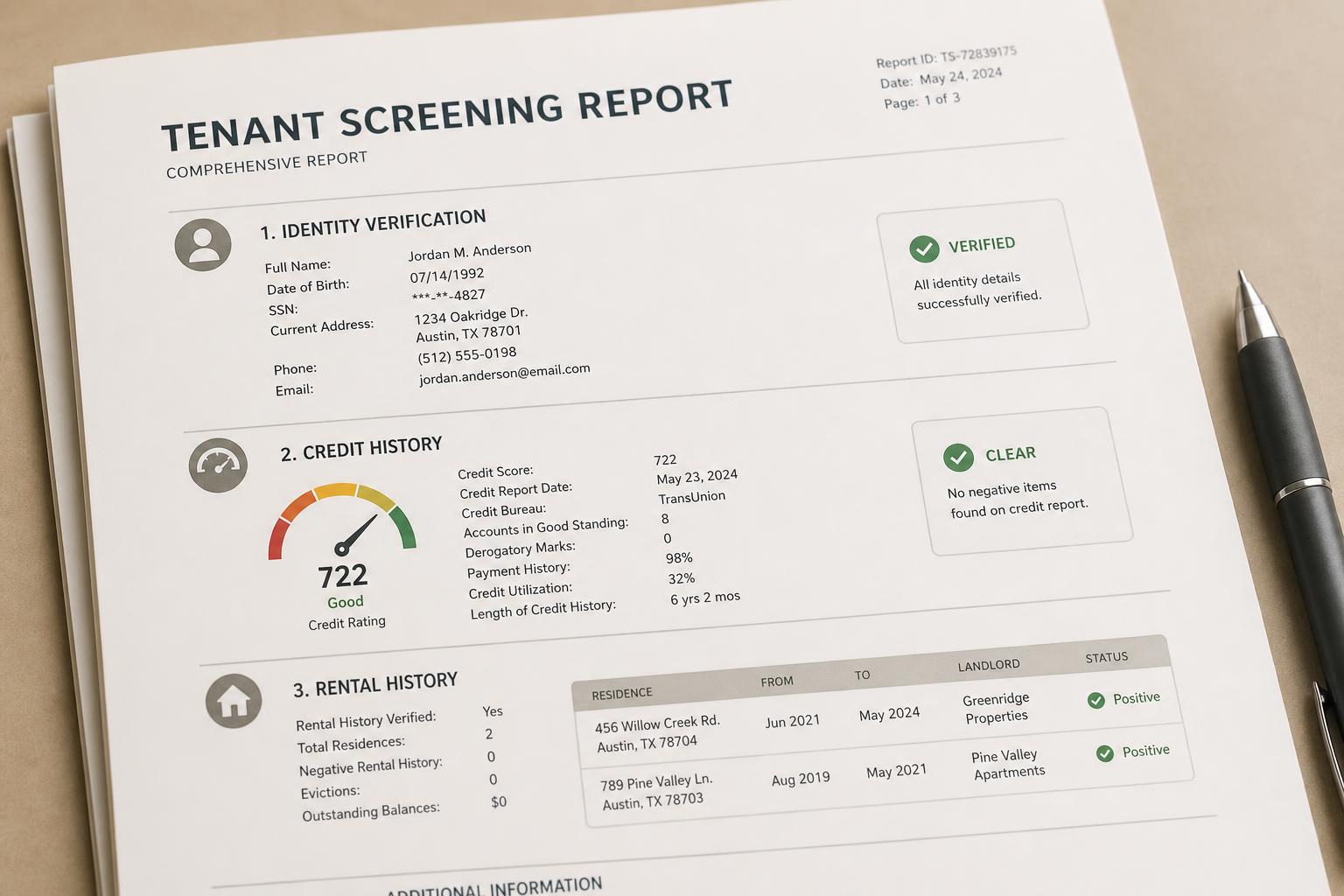

A tenant screening report is a consumer report a landlord buys to evaluate you. It isn’t a single document — it’s a compilation pulled from one or more screening companies, and it usually blends your credit information with rental history, public records, and sometimes a background check. Some reports add a recommendation or a risk score.

Because these companies are consumer reporting agencies under the FCRA, you have real rights: to know what’s in your file, to a copy, and to dispute anything inaccurate. The catch is that the report is built about you, not for you — so mistakes can sit there unseen until they cost you an apartment.

How do you get a copy of your own tenant screening report?

Two main paths. First, if you were denied based on a report, the landlord must send an adverse action notice naming the screening company — and you’re entitled to a free copy from that company. Second, you can request your file directly from the major tenant-screening agencies; the FCRA entitles you to a free file disclosure once every 12 months from each.

Requesting your own report before you start applying means no surprises — you see exactly what a landlord will see, with time to correct anything wrong.

Section by section: what’s actually in the report?

Reports vary by company, but most contain the same building blocks. Here’s how to read each one.

Identity & address history

Your name, past addresses, and sometimes date of birth. Check for addresses that aren’t yours or name variations — these are the first sign of a “mixed file,” where someone else’s data is blended with yours.

Credit information

A credit score or range, plus collections, balances, and payment patterns. Landlords read this for reliability. Confirm the accounts and balances are accurate and actually yours.

Rental & eviction history

Prior addresses, and any eviction filings or judgments. This is where errors are common — a dismissed case, a settled matter, or a record belonging to someone with a similar name can appear as if it’s an active eviction.

Public records & background

Some reports include criminal or public-record data. Accuracy and completeness matter here, and HUD guidance cautions landlords against blanket bans based on records. Check that anything listed is current, complete, and yours.

How do landlords use the score or recommendation?

Many screening products end with a recommendation — “accept,” “accept with conditions,” or “decline” — or a numeric score the landlord sets a cutoff against. A flexible landlord may read the underlying detail; an automated complex may just apply the cutoff. Knowing your report includes a recommendation explains why two landlords can treat the same history differently.

Why do tenant screening reports so often contain errors?

The Consumer Financial Protection Bureau (CFPB) has flagged tenant screening as error-prone. Reports are assembled quickly from multiple databases and matched on names and dates of birth — so people with common names get mixed files, old records resurface, and dismissed cases show up as live ones. Because you don’t normally see the report, these errors can repeat across applications until you catch and dispute them.

How do you dispute an error on a tenant screening report?

The FCRA gives you a clear process. Identify the screening company (the adverse action notice names it), then file a dispute directly with that company, in writing where possible, with documents that support your case — a court record showing a case was dismissed, proof of identity, or evidence an account isn’t yours.

The company generally must investigate, usually within about 30 days, and correct or remove information it can’t verify. This is about accuracy: you’re asking them to report the truth, not to erase something legitimate. If a record is accurate, the more useful step is understanding it and explaining its context to a landlord.

What can you do about an accurate but damaging record?

If the report is correct, you have different tools. Context helps: a brief, honest explanation of an old eviction or a past collection — and proof you’ve rented responsibly since — can move a flexible landlord. Strengthening the rest of your application (income, references, a larger deposit) gives them reasons to say yes despite the record. And addressing what’s on your credit over time changes future reports.

Should you check your report before you apply?

Almost always, yes. Application fees add up, and each denial can mean a wasted fee and an inquiry. Pulling your own tenant-screening and credit reports first lets you fix mistakes, prepare explanations, and apply where you actually stand a chance. A free 15-minute credit review walks you through what’s likely showing and what may be worth disputing.

Reading and acting on your report

Treat the report as a checklist, not a verdict.

Do

Don’t

Red flags in screening and “repair” offers

Where there’s a denial, there are bad offers. Watch for these.

Be cautious if you see

The bottom line on screening reports

The tenant screening report is the quiet decision-maker behind most rental applications — and it’s often wrong in small, consequential ways. Reading your own copy, disputing real errors, and preparing for accurate ones turns a black box into something you can manage.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

See what your report is saying before a landlord does

A free 15-minute review walks through what’s on your credit report — and what may be inaccurate or disputable — so you can apply prepared instead of guessing.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.