Renting after a denial

What Are Second Chance Apartments — and How Do You Qualify?

If an eviction, a broken lease, or a low credit score is standing between you and an apartment, a “second chance” rental may be an option. Here’s how they actually work — and how to put your strongest application forward.

Quick answer

Second chance apartments are rentals from landlords and property managers who will consider applicants with evictions, broken leases, collections, or poor credit — usually in exchange for a larger deposit, a co-signer, or stricter lease terms. They are not “no credit check” rentals; most still pull a tenant-screening report, but they weigh it more flexibly.

You improve your odds by knowing exactly what’s on your credit and tenant-screening reports before you apply, correcting anything inaccurate, and strengthening the parts of your application a landlord can say yes to — income, references, and a deposit.

Denied a rental, or facing a credit check? A free 15-minute review shows what’s actually on your report — and what to address first.

No credit card · phone optional · no obligation.

What is a second chance apartment?

“Second chance” isn’t an official category — it’s a label for landlords who don’t auto-reject an application the moment a screening report shows an eviction, a charge-off, or a thin credit file. Instead of a hard cutoff, they look at the whole picture: your income, your rental references, the reason behind a past problem, and your willingness to put down a larger deposit.

These are often independent landlords, smaller property-management companies, or specific communities that market themselves as “second chance” or “credit-flexible.” Larger complexes with rigid, automated screening are usually the ones issuing the denials in the first place. The trade-off is that flexibility tends to cost more — but with the right preparation, a second chance apartment can be a genuine bridge back to standard housing.

Second chance vs. “no credit check” apartments — what’s the difference?

They sound similar, but they’re not the same thing, and the difference matters for your wallet.

- A second chance apartment still checks your credit and history — it just considers applicants other landlords would reject. You’re being evaluated, not waved through.

- A “no credit check” apartment skips the credit pull entirely — and usually prices that risk back to you through higher rent, a bigger deposit, or weaker lease terms.

If you’re weighing a no-credit-check listing, it’s worth understanding the trade-offs first. We cover them in No Credit Check Apartments: What They Don’t Tell You. In many cases, a second chance apartment — or simply addressing what’s on your report — is the better-value path.

What do landlords actually check on a second chance application?

Even flexible landlords run some version of a screening process. Knowing what they look at tells you where to focus.

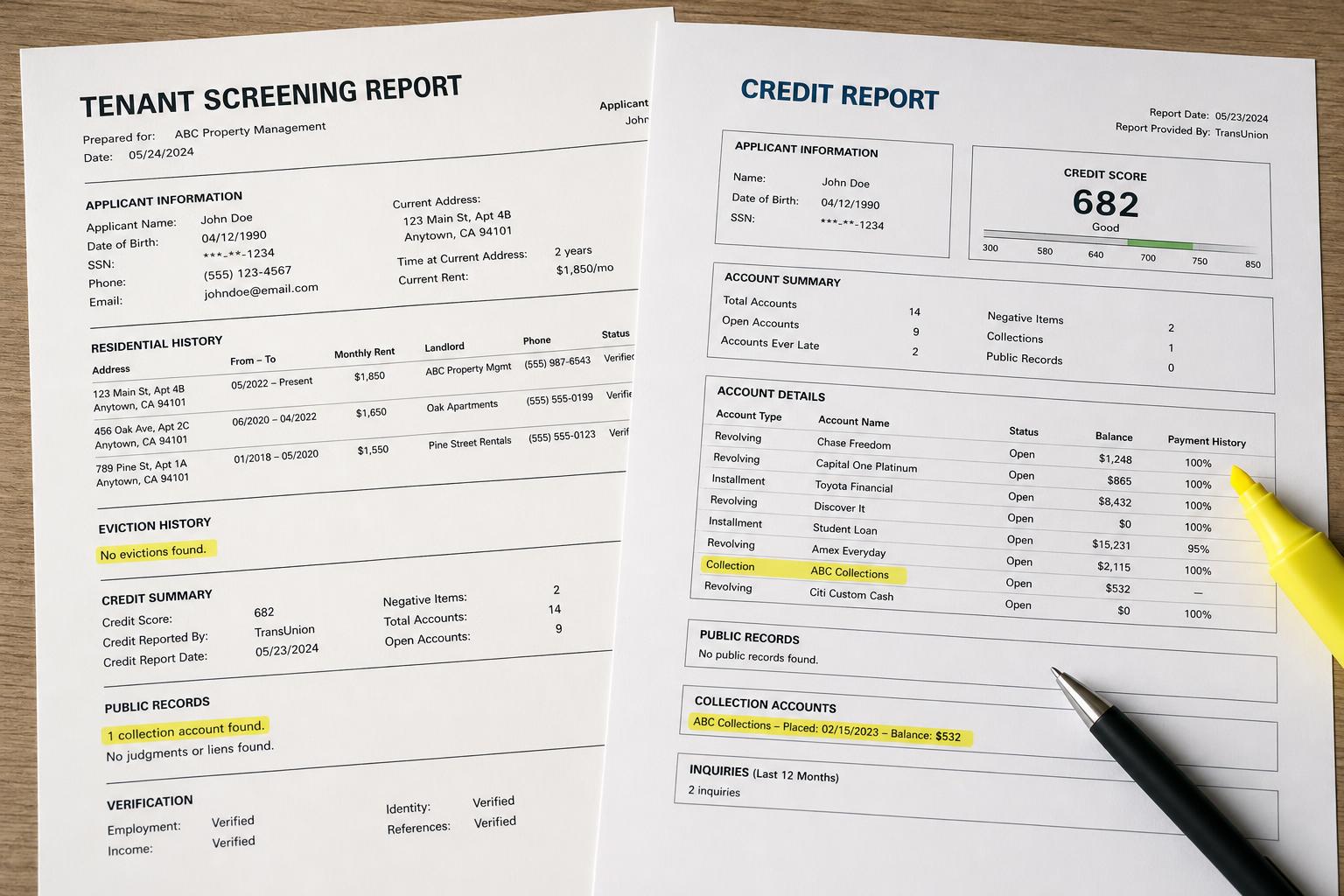

Your credit report and score

Many landlords pull credit to look for collections, charge-offs, and overall payment patterns. A few negative items can trigger an automatic “no” at a strict complex — but a second chance landlord may look past them if the rest of your application is strong.

Your tenant-screening report

This is separate from your credit report. Tenant-screening companies compile rental history, eviction records, and sometimes background information. Under the Fair Credit Reporting Act (FCRA), these companies are consumer reporting agencies — which means you have the right to see your report and to dispute anything inaccurate.

Income and employment

Most landlords want to see that your income comfortably covers the rent — a common rule of thumb is monthly income of about three times the rent. Steady, documented income is one of the strongest things you can bring to a second chance application.

Rental history and references

A reference from a previous landlord confirming you paid on time can carry real weight, especially if it offsets an older problem. If you don’t have a prior landlord to call on, character references and proof of consistent payments can help fill the gap.

What credit score do you need for a second chance apartment?

There’s no universal cutoff. Standard apartment communities often look for scores in the mid-600s or higher, but second chance landlords are precisely the ones willing to go lower — sometimes well into the 500s — when the rest of your application is strong. Some don’t lean on a score at all and instead read the report directly, looking at what the negative items are rather than a single number.

Because there’s no fixed number, the more useful question isn’t “what’s my score?” but “what’s actually on my report, and is any of it wrong?” An error you can correct, or context you can explain, often matters more to a flexible landlord than the score itself. A free 15-minute credit review shows you what a landlord is likely to see and where you stand before you apply.

Can you get a second chance apartment with an eviction on your record?

Often, yes — it’s the situation second chance rentals exist for. An eviction can appear on your tenant-screening report and, if it went to court or collections, may also surface elsewhere. But landlords vary widely in how they treat it.

A few things help: an eviction that’s several years old generally weighs less than a recent one; a documented explanation (a job loss, a medical emergency) gives context; and proof you’ve rented responsibly since then can reassure a landlord. It’s also worth confirming the eviction is being reported accurately — wrong dates, a case that was dismissed, or a record that isn’t yours are all things you can dispute under the FCRA.

How long does an eviction stay on your record?

Eviction-related information generally appears on tenant-screening and credit reports for up to seven years under the Fair Credit Reporting Act, though the specifics vary by state and by what was actually filed. An eviction that was dismissed, settled, or never completed may be reported differently — or shouldn’t appear at all.

Two things work in your favor over time. First, age: a years-old eviction with a clean record since carries far less weight with a flexible landlord than a recent one. Second, accuracy: if you find an eviction record that’s inaccurate, outdated, or not yours, you have the right to dispute it with the screening company that’s reporting it. Checking before you apply means you’re not blindsided by a record you could have corrected.

Can you qualify with bad credit or no credit?

Yes. Bad credit and no credit are different problems, but both are workable with a second chance landlord. With a low score, the goal is to show the score doesn’t tell the whole story — strong income, on-time rent elsewhere, and a willingness to put more down. With no credit history, the challenge is simply a lack of data; references, proof of income, and sometimes a co-signer help fill that gap.

Either way, the single most useful thing you can do is find out what a landlord actually sees when they pull your report — so you’re not guessing. Addressing accurate issues and disputing anything inaccurate can strengthen your profile over time, and it starts with seeing the report clearly.

What do second chance apartments cost?

Flexibility usually comes at a price. Expect one or more of the following:

- A larger security deposit — sometimes one and a half to two months’ rent instead of one.

- A higher monthly rent at some properties, to offset the perceived risk.

- A co-signer or guarantor requirement if your income or credit is thin.

- Stricter lease terms — a shorter initial term or a probationary period.

None of these is automatically a bad deal. The key is to compare the total cost — deposit plus rent plus any premium — against what you’d pay at a standard apartment if you addressed what’s on your report first.

Do second chance apartments report your rent to the credit bureaus?

Often they don’t. Most landlords — second chance or otherwise — don’t report your monthly rent payments to the credit bureaus, so paying on time may not directly build your credit the way many renters assume. If building credit matters to you, ask the landlord directly whether they report, or look into a third-party rent-reporting service that can add your on-time payments to your file.

The bigger point: don’t count on a “second chance” lease to rebuild your credit on its own. Pairing the lease with a plan to understand and address what’s actually on your report is what moves things in a lasting way.

How to qualify: ways to strengthen your application

You have more control over a second chance application than a standard one, because the landlord is looking for reasons to say yes. Give them those reasons.

Do

Don’t

Check your reports before you apply — and use your rights

If you were turned down for an apartment based on a report, the landlord is generally required to send you an adverse action notice naming the screening company they used. That notice is valuable: it points you to the exact company holding your file, and under the FCRA you can request a copy and dispute errors.

The Consumer Financial Protection Bureau (CFPB) notes that tenant-screening reports frequently contain mistakes — mismatched identities, records that belong to someone else, or outdated information. Catching those before you apply can be the difference between a yes and a no. A free rental credit review walks you through what’s reporting and what may be worth disputing.

How to spot second chance apartment scams

Where there’s urgency, there are scams. The FTC warns that rental fraud often targets people who feel they have limited options. Watch for these:

Red flags before you pay anything

Are second chance apartments worth it?

It depends on your timeline. If you need a place now, a fair second chance apartment can be a genuine solution — a real lease, a real address, and breathing room. The risk is treating it as a permanent fix: paying a long-term premium for a short-term problem.

The stronger long game is to use the time in a second chance unit to understand and improve what’s on your credit, so your next application can be a standard one with standard terms.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

Apply with a plan, not a guess

A free 15-minute review shows you what’s on your credit report behind a rental denial — and a realistic next step before you apply again.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.