The First Three Things to Check After a Denial

Getting turned down — for an apartment, a loan, a credit card, or a better insurance rate — is frustrating and feels personal. But a denial is rarely the end of the road. It’s a signal, and usually something you can work on. Here are the first three things to check.

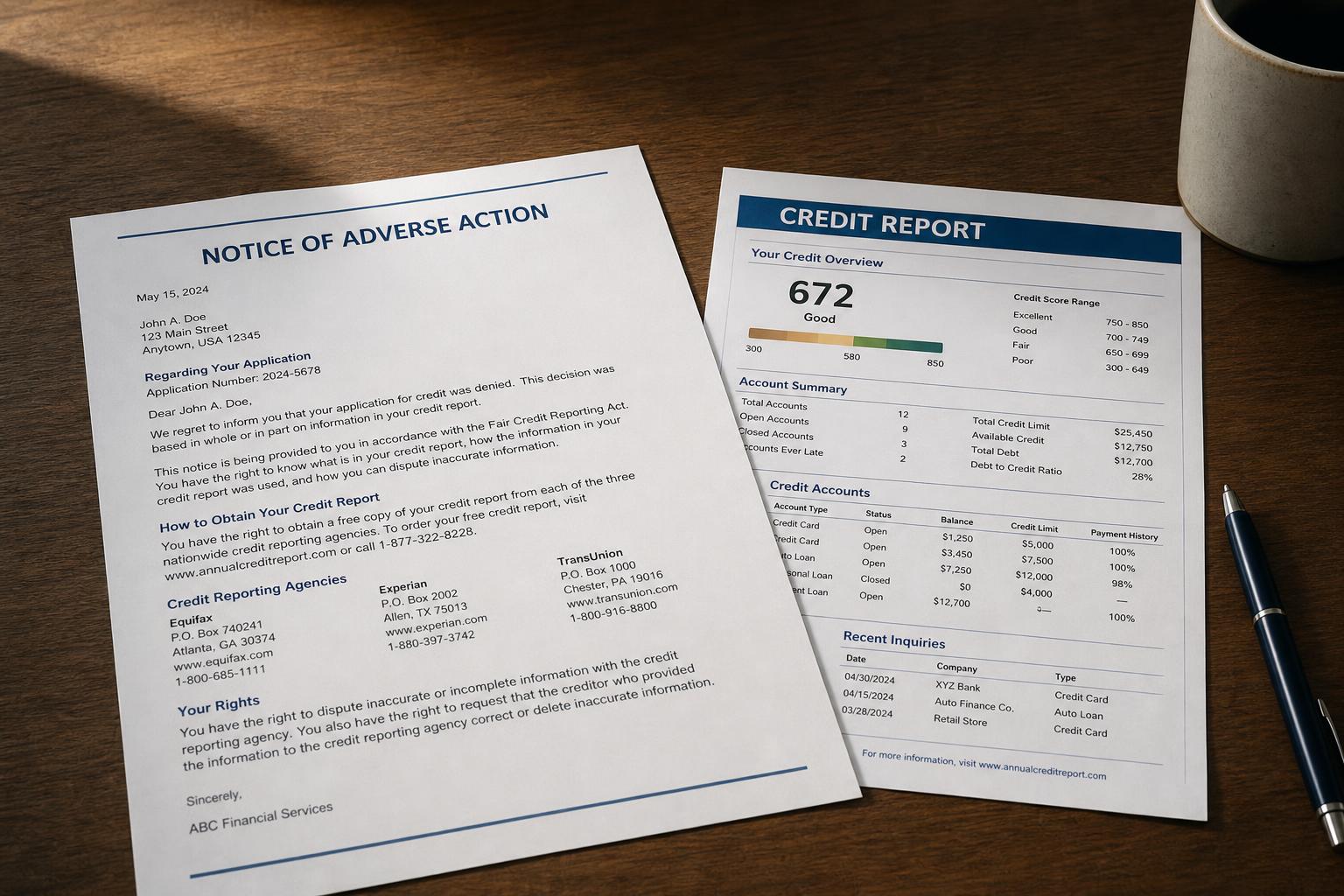

1. Get the reason in writing

By law, when you’re denied based on your credit, the company must send you an adverse action notice telling you why and which credit bureau they used. If you didn’t get one, ask. This single document points you straight at what’s holding you back.

2. Pull your actual credit report

After a denial you’re entitled to a free copy of the report used in the decision. Pull all three bureaus at AnnualCreditReport.com — the only official source. Don’t rely on a credit-score app; it won’t show what lenders and landlords actually see.

3. Find the 2–3 items doing the damage

Most denials come down to just a few negative items: collections, late payments, high balances, or outright errors (the FTC found about 1 in 5 consumers had one). Identify them, and you’ve found your to-do list.

From there, the path depends on what you’re facing:

Not sure where to start? A free 15-minute consultation will tell you exactly what’s on your report and what you can do about it — no cost, no obligation.

Sources: Federal Trade Commission (FTC) — credit-report accuracy (the 1-in-5 study) and adverse-action rights; Consumer Financial Protection Bureau (CFPB) — disputing errors and pulling your reports; AnnualCreditReport.com. General education, not financial or legal advice.