How to Dispute an Error on Your Credit Report

Credit-report mistakes are more common than most people realize — and you have a clear, free right to fix them. Here’s the step-by-step.

A wrong account, a balance that isn’t yours, a paid debt still marked unpaid — errors like these quietly cause denials every day. Studies and the CFPB’s own complaint data show credit-report mistakes are widespread.

The Fair Credit Reporting Act (FCRA) gives you the right to dispute anything inaccurate and have it investigated — for free. Here’s how to do it properly.

Why credit-report errors are so common

Your credit file is assembled automatically from data sent by many creditors and matched to you by name, address, and Social Security number. That speed creates mistakes: accounts get attached to the wrong person (a mixed file), old debts resurface, paid balances don’t update, and identity theft adds accounts you never opened. None of it is your fault — but catching it is your job, because no one else is checking for you.

Step 1: Get all three of your reports

Start by pulling your reports from all three bureaus — Equifax, Experian, and TransUnion — free and weekly at AnnualCreditReport.com, the only federally authorized source. Review each one, because an error can appear on one bureau and not the others.

If you were denied based on a specialized report, like a tenant screening report, you can request that file too.

Step 2: Identify what actually counts as an error

Disputes are for inaccurate, incomplete, or unverifiable information. Common valid examples:

- An account that isn’t yours, or you never opened

- A wrong balance, credit limit, or payment status (e.g., a paid debt shown unpaid)

- A late payment you actually made on time

- A duplicate of the same debt, or one reporting past its date

- Incorrect personal information that may be merging your file with someone else’s

What doesn’t count: accurate negative items you simply wish weren’t there. More on that below.

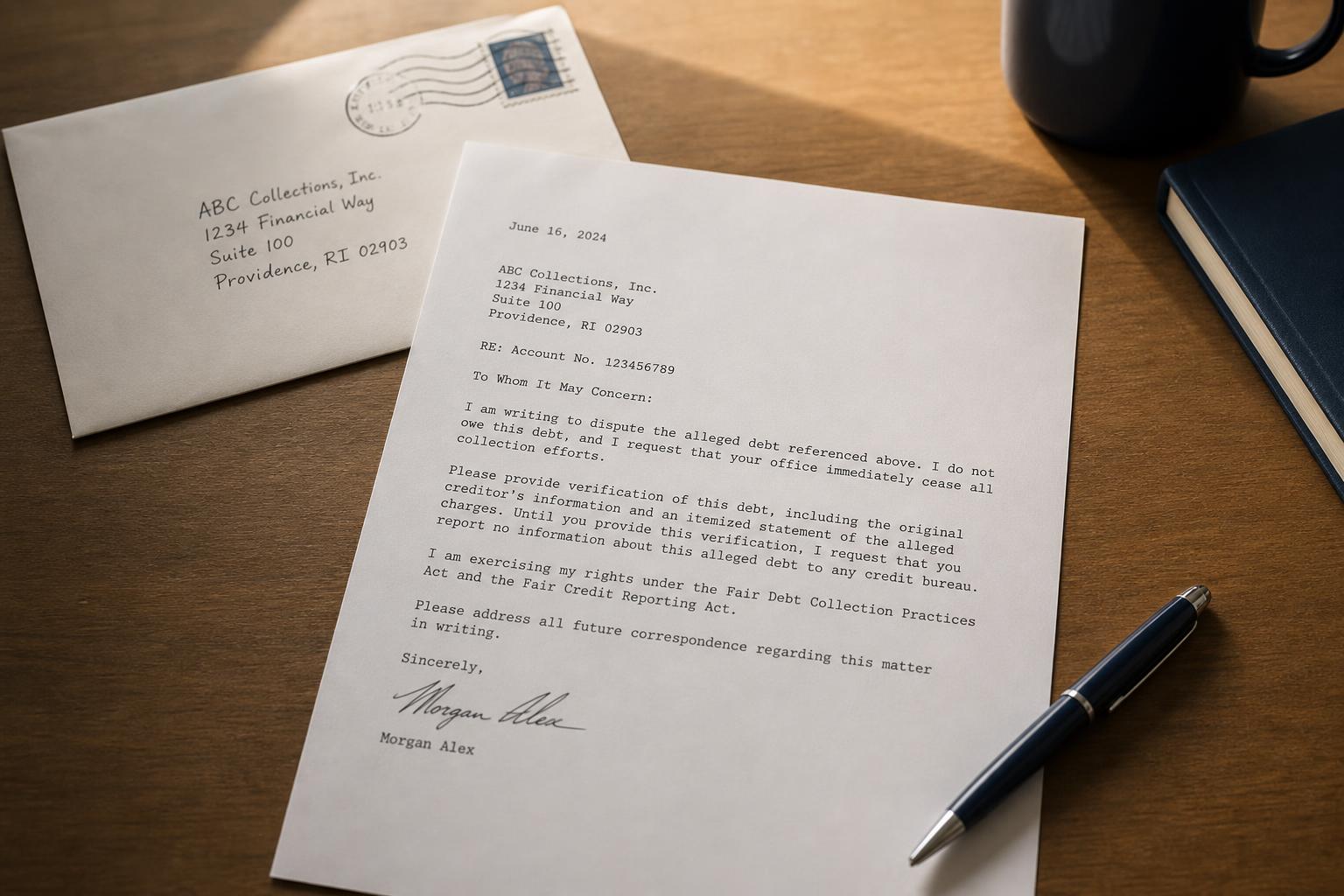

Step 3: File the dispute — with the bureau and the furnisher

You have two channels, and using both is strongest:

- The credit bureau that’s reporting the error (online, by mail, or by phone). They must investigate.

- The furnisher — the bank, lender, or collector that supplied the information — which also has obligations to investigate disputes.

Putting it in writing creates a paper trail; sending by certified mail gives you proof of the date.

Step 4: Include the right documentation

A dispute is far stronger with evidence. Include:

- A clear statement of what’s wrong and what it should say

- A copy of the report with the item circled

- Supporting proof — a payoff letter, bank statement, court record, or identity documents

- Your contact information and the account or reference number

Keep copies of everything you send.

Step 5: The ~30-day investigation

Once you file, the bureau generally must investigate and respond within about 30 days (sometimes up to 45). They contact the furnisher, review what you submitted, and must correct or delete information that can’t be verified. You’ll get the results in writing, and if something changes, you’re entitled to a free updated report.

If it’s not fixed

If the bureau says the item was “verified” but you still believe it’s wrong, you have options: ask for the method of verification, re-file with additional evidence, add a brief statement of dispute to your file, and file a complaint with the Consumer Financial Protection Bureau (CFPB), which forwards it to the company for a response. Persistent, documented follow-up is what resolves stubborn errors.

An honest caveat: disputes are for errors

The dispute process exists to make your report accurate — not to erase legitimate history. Accurate negative items can’t be disputed away, and any company promising to “delete” true, verifiable accounts is selling something it can’t deliver (and may be skirting the law). For accurate items, the real path is the slower one — addressing the debt and building positive history — including for medical collections, which follow their own rules.

Key takeaways

- Credit-report errors are common because files are assembled automatically and matched imperfectly.

- Pull all three reports free at AnnualCreditReport.com and review each separately.

- Dispute only inaccurate, incomplete, or unverifiable items — with the bureau and the furnisher.

- Include documentation; the bureau generally must investigate within about 30 days.

- If it’s not fixed, escalate to the CFPB — but accurate records can’t be disputed away.

Think something on your report is wrong?

A free 15-minute review helps you spot what may be inaccurate or out of date across all three bureaus — so you know exactly what’s worth disputing.

Free · about 15 minutes · no credit card · no obligation.

Sources: Fair Credit Reporting Act (FCRA) — your right to dispute and the investigation timeline; Consumer Financial Protection Bureau (CFPB) — how to dispute errors and file a complaint; Federal Trade Commission (FTC) — correcting credit-report errors. Timelines and procedures can vary; this is general education, not legal advice.