How Credit Scores Actually Work: The 5 Factors

A denial often traces back to a three-digit number most people have never had explained to them. Here is what actually goes into a credit score — and what doesn’t.

When you’re turned down for an apartment, a car loan, or a better insurance rate, the decision usually comes down to a credit score you’ve probably never seen broken apart. It can feel like a black box. It isn’t.

A credit score is built from a handful of factors, and once you know what they are, the number stops being mysterious and starts being something you can act on. Here’s the plain-English version.

What is a credit score, really?

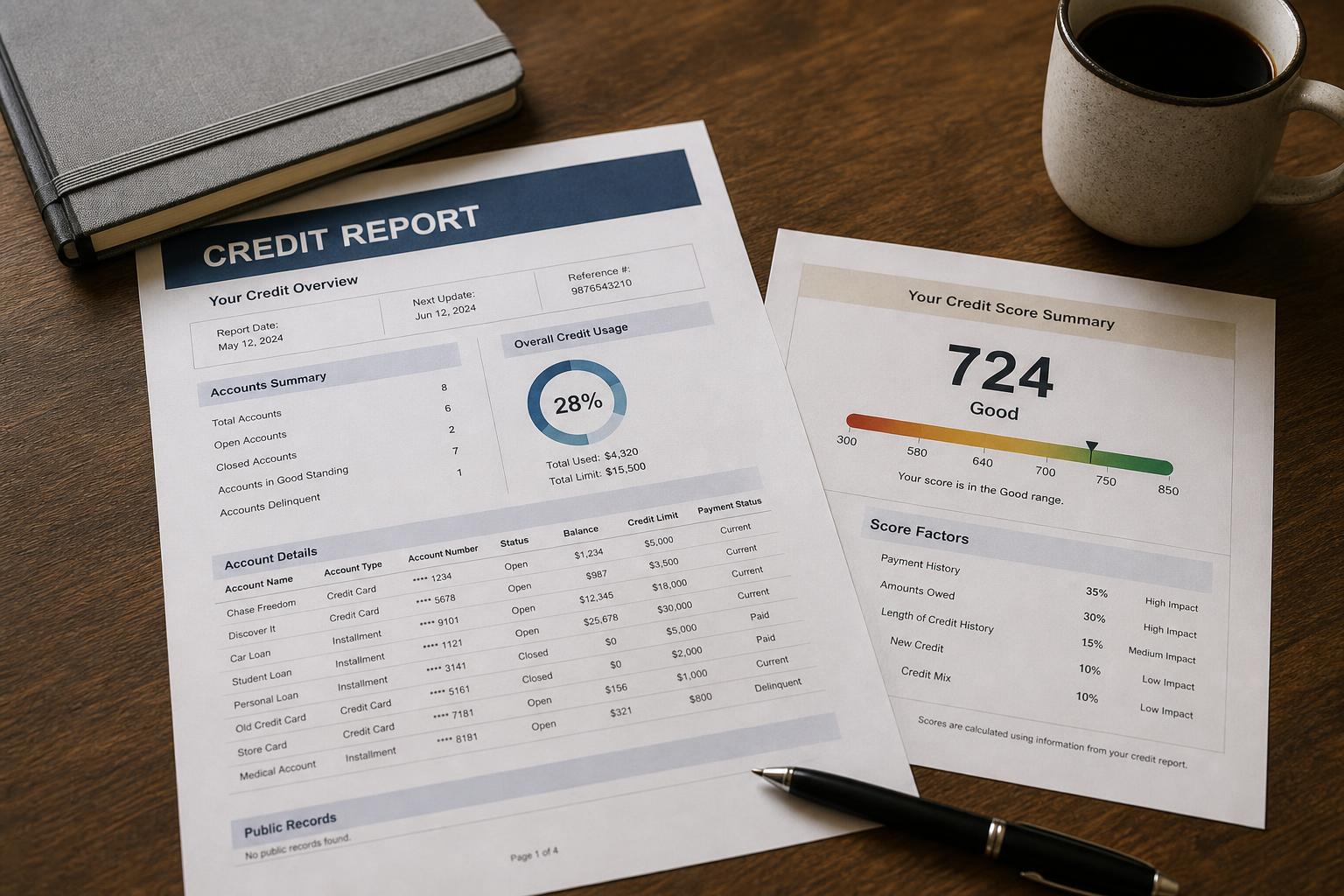

A credit score is a three-digit number — most commonly on a 300–850 scale — that estimates how likely you are to repay borrowed money on time. Lenders, landlords, and (in most states) insurers use it as a fast read on risk.

It’s calculated from the information in your credit reports at the three nationwide bureaus — Equifax, Experian, and TransUnion. Change what’s in the reports and the score follows.

Why you have more than one score (FICO vs. VantageScore)

There isn’t a single official score. Two companies dominate: FICO and VantageScore. Both read the same report data, but they weigh it a little differently and update their formulas over time — so you actually have many scores, and they rarely match exactly.

Which one a lender sees depends on the lender and the type of credit. That’s normal. Don’t chase a specific number; focus on the underlying report, because every model is reading from it.

The 5 factors — and roughly how much each counts

FICO publishes general weightings for the broad population. Yours can differ, but the order almost never does:

- Payment history — about 35%. Have you paid past accounts on time?

- Amounts owed / utilization — about 30%. How much of your available credit you’re using.

- Length of credit history — about 15%. How long your accounts have been open.

- New credit — about 10%. Recent applications and newly opened accounts.

- Credit mix — about 10%. The variety of credit you manage.

VantageScore describes these as levels of influence rather than fixed percentages, but the same two factors — payment history and utilization — do most of the work in every model.

Payment history: the one that moves the needle most

This is the biggest factor for a reason: the strongest predictor of future payment is past payment. A single payment reported 30 or more days late can hurt, and the more recent and more severe the miss, the heavier it weighs. Collections, charge-offs, and bankruptcies live in this category too.

The encouraging part: it’s also the factor most within your control going forward. Every on-time payment from here adds positive history, and negative marks lose weight as they age before they eventually fall off (see how long negative items stay on your report).

Amounts owed: mostly your credit utilization

The second-biggest factor is driven largely by credit utilization — the share of your revolving limits (credit cards, lines of credit) that you’re currently using. As a rule, lower is better, and it updates as your balances move, so this is one of the more responsive levers you have.

The widely repeated “keep it under 30%” advice is an oversimplification. We unpack what actually helps in credit utilization and the “30% rule” myth.

Length, new credit, and mix: the supporting cast

The last three factors matter less individually, but they add up:

- Length of history looks at the age of your oldest account and the average age of all of them. Older is better — which is why closing your oldest card, or opening several new ones, can quietly drag the average down.

- New credit reflects recent applications. Each application can add a hard inquiry, and several in a short window can look risky (here’s the difference between soft and hard inquiries).

- Credit mix rewards handling both revolving accounts (cards) and installment accounts (loans). It’s a minor factor — never take on debt you don’t need just to “improve your mix.”

What is NOT in your credit score

Plenty of things people assume matter don’t appear in your FICO or VantageScore at all:

- Your income, savings, or bank-account balance

- Your job or employment history

- Your age, race, religion, national origin, sex, or marital status — using these in lending is prohibited under the Equal Credit Opportunity Act

- Where you live

- Checking your own credit (that’s a soft inquiry, with no effect)

So “I have a good job” doesn’t directly raise your score. Income still matters to a lender or landlord — just separately from the score itself.

How to see what’s affecting your own score

Start with the source. You can pull all three credit reports for free, weekly, at AnnualCreditReport.com — the only federally authorized site. Many banks and card issuers also show a score and its top influencing factors for free.

If you were recently denied, the adverse action notice you received lists the specific reasons that weighed most. That notice, read against your report, usually points straight at the one or two factors holding you back.

Key takeaways

- A credit score predicts repayment risk and is built entirely from your credit-report data.

- You have many scores (FICO and VantageScore, multiple versions) — the underlying report is what they all read.

- Payment history (~35%) and utilization (~30%) drive most of the score.

- Income, employment, age, and protected characteristics are not in your score.

- Pull your free reports and read your adverse-action notice to see what’s affecting yours.

See what’s actually affecting your score

A free 15-minute review walks through what’s on your credit report and which factors are weighing on your score — so you know exactly where to focus.

Free · about 15 minutes · no credit card · no obligation.

Sources: Consumer Financial Protection Bureau (CFPB) — how credit scores work and what affects them; FICO and VantageScore — published scoring-factor guidance; Equal Credit Opportunity Act (ECOA) — prohibited bases in lending. Scoring models and weightings vary; this is general education, not financial or legal advice.