Medical debt & credit

Do Paid Medical Collections Still Show on Your Credit Report?

You paid the medical collection — so why is it still on your report? Here’s what should happen under the current rules, and what to do if it’s lingering.

Quick answer

Generally, no — paid medical collections should not appear on your credit reports. The national credit bureaus stopped including them, so once a medical collection is paid, it should drop off.

If a paid medical collection is still showing, it’s most likely a reporting error or an update that hasn’t caught up — and that’s something you can dispute and get corrected.

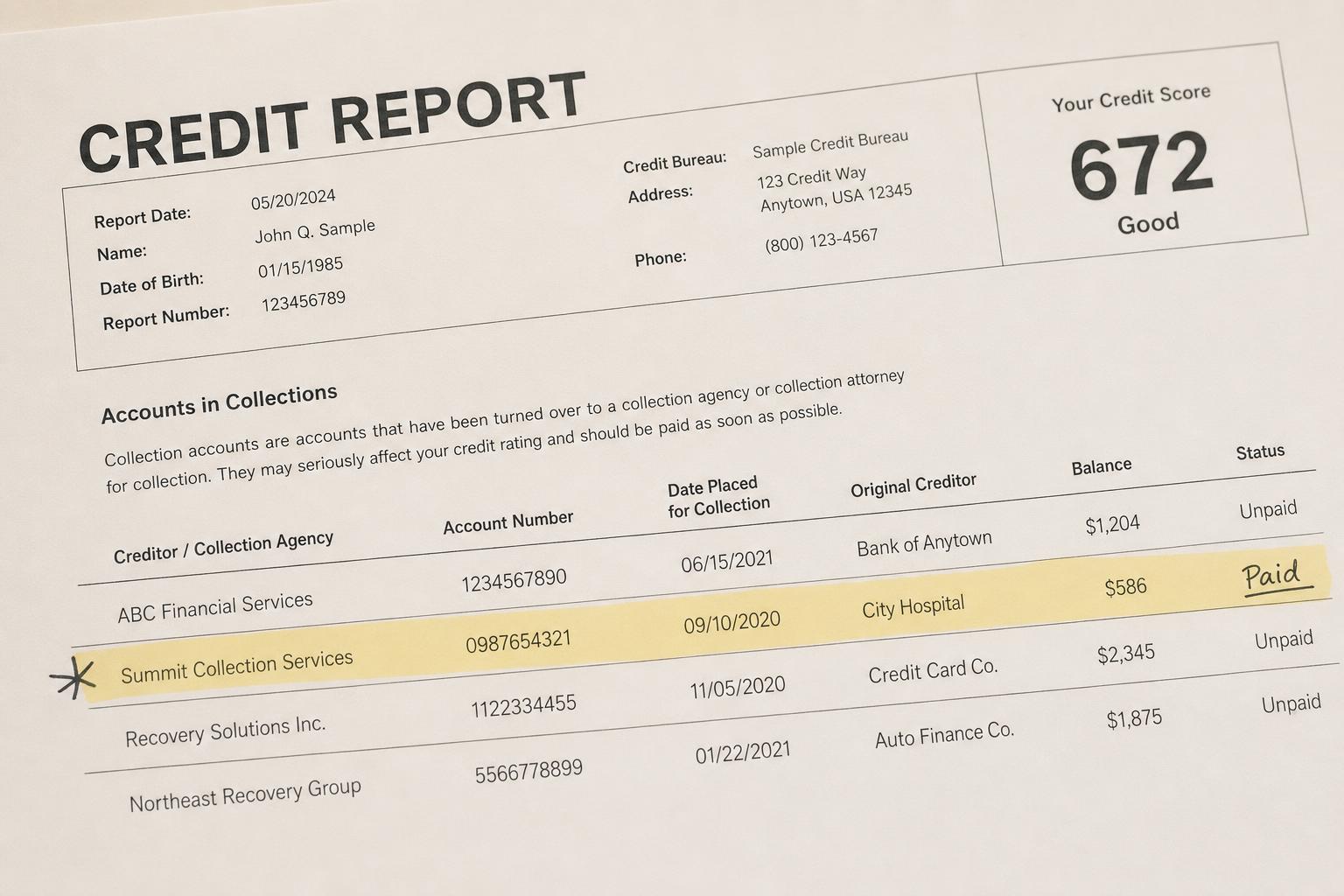

Should a paid medical collection still be on my report?

No. As part of the bureaus’ medical-debt changes, paid medical collections are removed from credit reports at Equifax, Experian, and TransUnion. So a medical collection you’ve fully paid should no longer be listed — and shouldn’t be weighing on your score.

Why is my paid medical collection still showing?

Usually one of a few reasons:

- Reporting lag — the collector or bureau hasn’t updated yet (it can take a billing cycle or two).

- A data error — the account wasn’t marked paid, or is duplicated.

- It’s on one bureau but not another — updates don’t always happen in sync.

None of these means you’re stuck — they’re all correctable.

How to dispute a paid medical collection that’s still there

Gather your proof of payment — a receipt, a paid statement, or a settlement letter — and file a dispute with each bureau still showing it, under the Fair Credit Reporting Act (FCRA). Point out that paid medical collections are no longer reported. The bureau must investigate, and with clear proof of payment these disputes are often straightforward.

Does paying a medical collection help your credit?

With the current rules, paying a medical collection should lead to its removal, which is better than just marking it paid. On newer scoring models, paid collections were already ignored; on older models still used by some lenders, removal is what actually helps. Either way, paying and then confirming it’s gone is the goal.

What about a settled or partially paid collection?

If you settled for less than the full amount, confirm how the collector agreed to report it and get that in writing before you pay. A balance reported as “settled” can read differently than “paid in full,” and you want the outcome documented so you can enforce it if the report doesn’t match.

How long should it take to come off after paying?

There’s no fixed deadline, but updates typically appear within a billing cycle or two. If a paid medical collection is still showing a couple of months later, that’s your cue to dispute it with proof of payment rather than wait indefinitely.

What to do if the dispute doesn’t fix it

If a bureau’s investigation doesn’t correct an obvious error, you can escalate: add a statement to your file, re-dispute with additional documentation, or file a complaint with the CFPB. A free review can help you confirm what’s reporting across all three bureaus and what to challenge.

Do paid medical collections affect a mortgage or rental application?

They shouldn’t — once removed under the bureau rules, a paid medical collection isn’t on the report a lender or landlord pulls. The catch is timing and consistency: if the removal hasn’t processed, or one bureau still shows it, it could surface at the wrong moment. Before a big application, confirm the paid collection is gone from all three reports. If you’re renting, our guide on renting with collections on your credit covers how landlords weigh them.

Should you pay a medical collection in full or settle?

It depends on the goal. Under the bureau rules, a medical collection should come off once it’s paid — so paying in full and confirming removal is the cleanest outcome. Settling for less resolves the balance for less money, but get in writing exactly how the account will be reported afterward (“paid” vs. “settled” can read differently). Either way, verify the debt is accurate and actually yours before you send a dollar.

Can a removed medical collection come back?

It generally shouldn’t, but it can happen — a collector who buys or re-reports a debt can cause a deleted item to reappear (“re-insertion”). The Fair Credit Reporting Act limits this: a furnisher generally must notify you before re-inserting a previously deleted item. If a paid or removed medical collection shows up again, treat it as an error, pull your proof, and dispute it again — you shouldn’t have to re-clear the same debt twice.

Paid medical collections: do’s and don’ts

Do

Don’t

The bottom line

A paid medical collection shouldn’t be on your report — period. If one is, it’s almost always a correctable error: gather your proof of payment and dispute it. You shouldn’t carry the weight of a debt you’ve already cleared.

Key takeaways

Before you pay or settle a medical bill, confirm what’s actually reporting. A free 15-minute review shows what may be inaccurate, outdated, or disputable — before you act. See the free medical-debt review →

Confirm it’s really gone — free review

A free 15-minute review helps you check what’s reporting across all three bureaus and what to dispute — so a debt you’ve paid isn’t still costing you.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.