Medical debt & credit

Medical Debt Under $500: Does It Hurt Your Credit?

Small medical collections are treated differently from large ones. Here’s what the under-$500 rule means for your credit — and why a small bill still deserves attention.

Quick answer

Under the credit bureaus’ rules, medical collections under $500 are no longer included on your credit reports. So a sub-$500 medical collection generally shouldn’t be affecting your score — and if one is showing, it’s likely a reporting error you can dispute.

That said, “not on your credit” isn’t the same as “gone.” A small unpaid medical bill can still go to collections, accrue, or be pursued — so it’s worth handling, just not panicking over what it does to your score.

Medical bills in collections? A free 15-minute review shows what’s actually reporting — and what may be inaccurate or disputable.

No credit card · phone optional · no obligation.

Does medical debt under $500 affect your credit?

Generally, no. As part of the bureaus’ medical-debt changes, Equifax, Experian, and TransUnion stopped including medical collections under $500. A small medical collection that follows this rule simply isn’t on your credit report, so it isn’t dragging down your score.

The under-$500 rule, explained

The threshold applies to the balance of the individual medical collection as reported. Collections below that amount are no longer added, and existing ones below it were removed. It’s one of three consumer-friendly bureau changes — alongside removing paid medical collections and waiting about a year before any unpaid medical collection can appear.

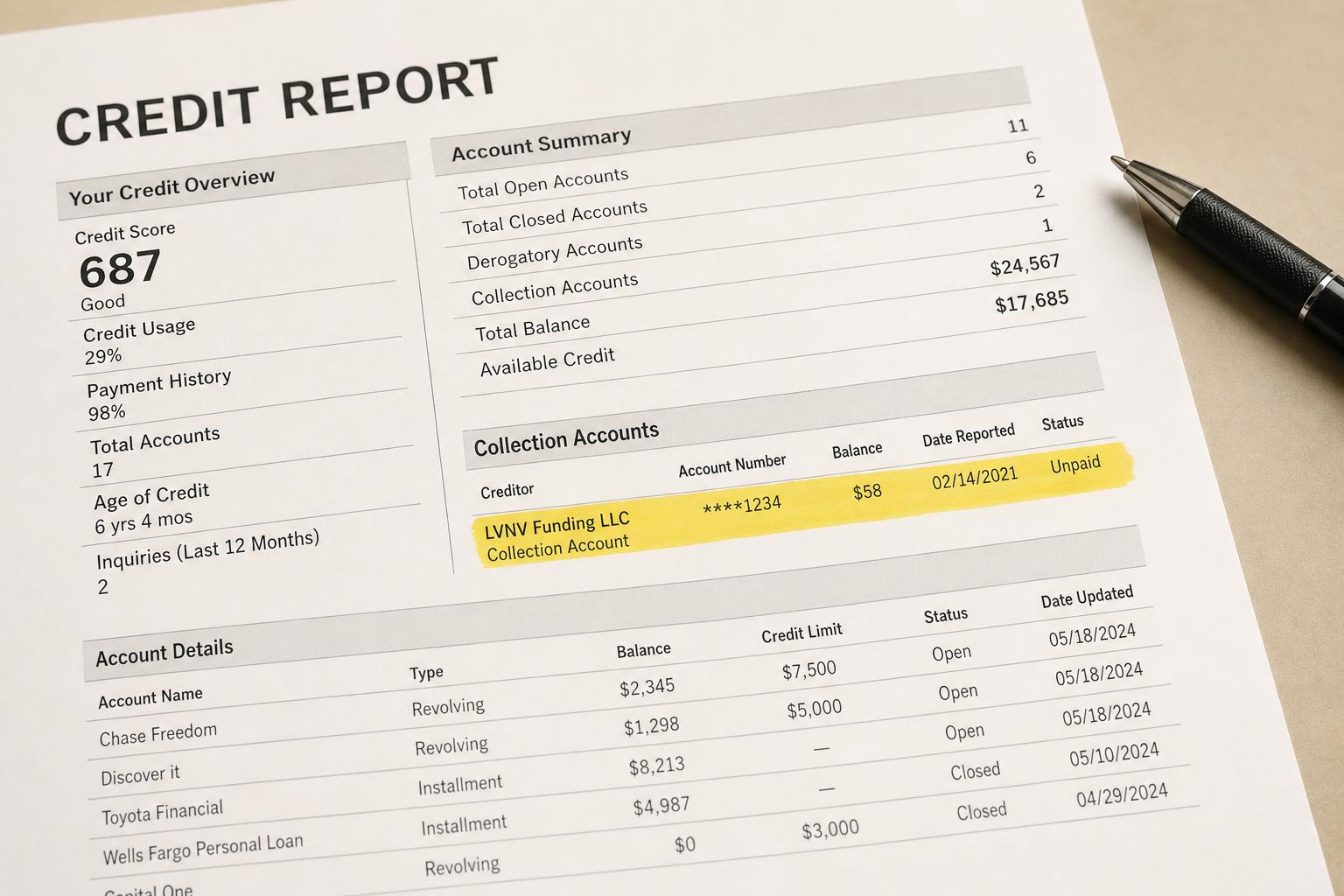

Why is a small medical collection still on my report?

If a medical collection under $500 is still listed, it’s most likely an error or an out-of-date entry. Gather any documentation and dispute it with the bureau under the Fair Credit Reporting Act (FCRA), noting that medical collections below $500 are no longer reported. With a clear case, these disputes are usually straightforward.

Does the $500 threshold combine multiple bills?

The threshold generally looks at each reported collection on its own, not a running total of every medical bill you have. Several separate small collections are each evaluated individually. If you’re unsure how a particular account is being reported, your credit report shows the balance the bureau is using — which is what determines whether it should appear.

What about medical debt over $500?

Larger unpaid medical collections can still be reported — but only after the roughly one-year waiting period, and not once they’re paid. If you’re dealing with a bigger balance, our guide Do Medical Bills Affect Your Credit Score? walks through the full set of rules and your options.

How long does small medical debt stay on your report?

If it follows the rule, a sub-$500 medical collection shouldn’t be on your report at all — so the better question is whether it’s there in error. Any medical collection that does report can otherwise remain up to seven years from the original delinquency, but the under-$500 and paid rules frequently take it off sooner.

Should you still pay a small medical bill?

Usually, yes — just for different reasons than your credit score. Even when it won’t appear on your report, an unpaid bill can still be sent to collections, generate calls, or in some cases be pursued in court. Confirm the bill is accurate against your insurance explanation of benefits first, then handle it — ideally before it ever reaches a collector.

Can a medical debt under $500 still go to court?

Yes. Keeping a debt off your credit report doesn’t make it disappear — a provider or collector can still pursue an unpaid medical bill, and in some cases that includes a lawsuit, regardless of the amount. The dollar threshold is about credit reporting, not collectability. That’s why it’s still worth confirming a small bill is accurate and resolving it, even though it isn’t denting your score.

Does the $500 count the bill or the collection balance?

It’s the balance of the collection account as reported — not the original bill, and not your total medical debt. A single collection under the threshold shouldn’t appear; a larger one can (after the waiting period, until paid). If you’re unsure, your credit report shows the balance the bureau is using for each account, which is what determines whether it qualifies for removal.

Do several small bills from one visit get combined?

Generally each collection account is evaluated on its own, so separate small balances are each measured against the threshold individually rather than summed. That said, a provider or collector could bundle multiple charges into one larger account that crosses $500. If that happens and you think the charges shouldn’t be grouped — or any of them is inaccurate — it’s worth questioning, since how the debt is packaged affects whether it reports at all.

Small medical debt: do’s and don’ts

Do

Don’t

The bottom line

A medical collection under $500 shouldn’t be touching your credit at all under the current rules. If one is, dispute it. And don’t confuse “off your credit report” with “handled” — a small bill is still worth resolving, just not worth losing sleep over.

Key takeaways

Before you pay or settle a medical bill, confirm what’s actually reporting. A free 15-minute review shows what may be inaccurate, outdated, or disputable — before you act. See the free medical-debt review →

Make sure a small bill isn’t wrongly on your report — free

A free 15-minute review helps you confirm what’s actually reporting and dispute any small medical collection that shouldn’t be there.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.