Renting with collections

Can You Rent an Apartment With Collections on Your Credit?

A collection account on your report can spook a landlord — but it’s rarely an automatic no. Here’s how collections affect a rental application, and how to apply with confidence.

Quick answer

Yes — you can often rent an apartment with a collection on your credit. Landlords care most about whether you’ll pay rent reliably, so the type of collection (rent or utility vs. medical), how old it is, and the strength of the rest of your application usually matter more than its mere presence.

Before you apply, confirm the collection is being reported accurately — many aren’t — and know what a landlord will see, so you can address or explain it up front instead of being caught off guard.

Do collections affect a rental application?

They can, but not all the same way. A landlord pulls your credit and tenant-screening reports to gauge one thing: how likely you are to pay rent on time. A collection is a yellow flag — not always a red one. What it signals depends on what kind of debt it is and how the rest of your application looks.

A strong income, clean recent rental history, and a willingness to explain the collection often outweigh the account itself — especially with the kind of flexible landlord who runs a second chance apartment.

Which collections matter most to landlords?

Landlords tend to weigh collections roughly like this:

- Prior landlord or rent debt — the biggest concern, because it speaks directly to paying rent.

- Utility collections — also relevant, since utilities are a recurring household obligation.

- Medical collections — generally weighed more lightly, and reporting rules have shifted so that many no longer appear or are removed once paid.

- Old, small, or one-off collections — usually less of a concern than recent, large, or rent-related ones.

Knowing which bucket yours falls into tells you how much explaining you’ll need to do.

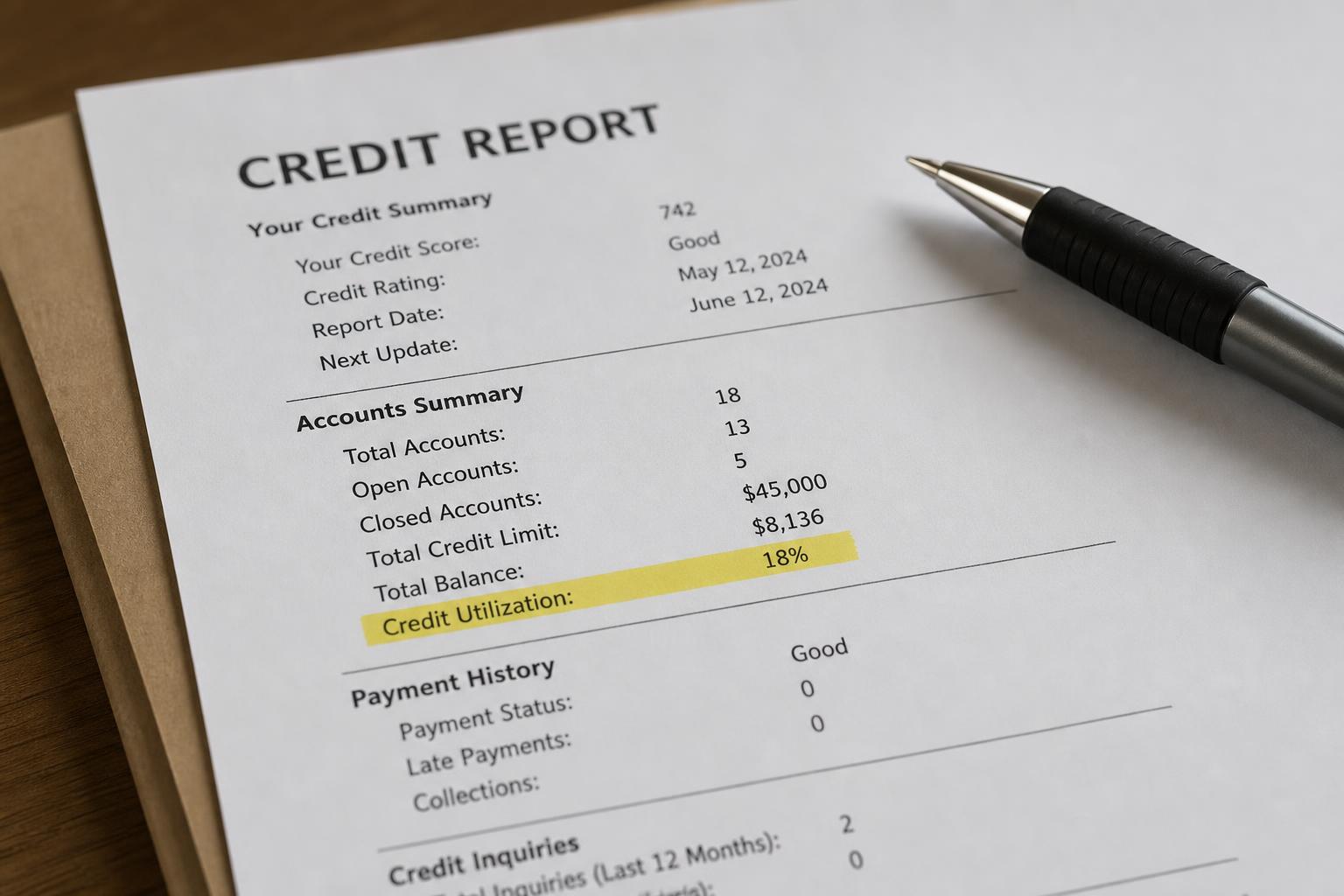

Are the collections even accurate? Check first

Before you assume a collection is a problem, confirm it’s correct. The Consumer Financial Protection Bureau (CFPB) reports that errors are common, and under the Fair Credit Reporting Act (FCRA) you can dispute anything inaccurate. Watch for:

- A balance that’s wrong or already paid.

- A duplicate of the same debt reported twice.

- An account that isn’t yours, or is from identity theft.

- A debt that’s being “re-aged” to look more recent than it is.

A free rental credit review helps you see what’s actually reporting and what may be disputable — before a landlord sees it.

Should you pay off a collection before applying?

It depends, and it’s worth thinking through rather than paying on reflex. Paying a collection doesn’t automatically remove it from your report, and on older scoring models a paid collection can still be visible. That said, a paid or settled rent/utility collection can reassure a landlord more than an open one.

If you do negotiate, get any agreement — including how the account will be reported afterward — in writing before you pay. And confirm the debt is valid and within your state’s limits first; paying can sometimes restart a clock you didn’t mean to restart.

How to get approved with a collection on your report

Preparation does the heavy lifting:

- Be upfront. Mention the collection before the landlord finds it, with a short, honest explanation.

- Bring proof of income — ideally around three times the rent — and recent on-time payment history.

- Offer a larger deposit or a co-signer to offset the perceived risk.

- Target flexible landlords — independents and second-chance properties weigh context, not just a score.

- Provide references from a prior landlord or employer.

How long do collections stay on your credit report?

Most collection accounts can remain on your credit report for up to seven years from the original delinquency date, under the Fair Credit Reporting Act. Paying a collection doesn’t reset or necessarily remove it — though it may then show as “paid,” which can read better to a landlord than an open balance.

Medical collections are an exception that’s been changing: industry and rule shifts have removed paid medical collections and many smaller balances from reports, and the rules continue to vary. If a collection is older than seven years and still showing, that’s an error you can dispute.

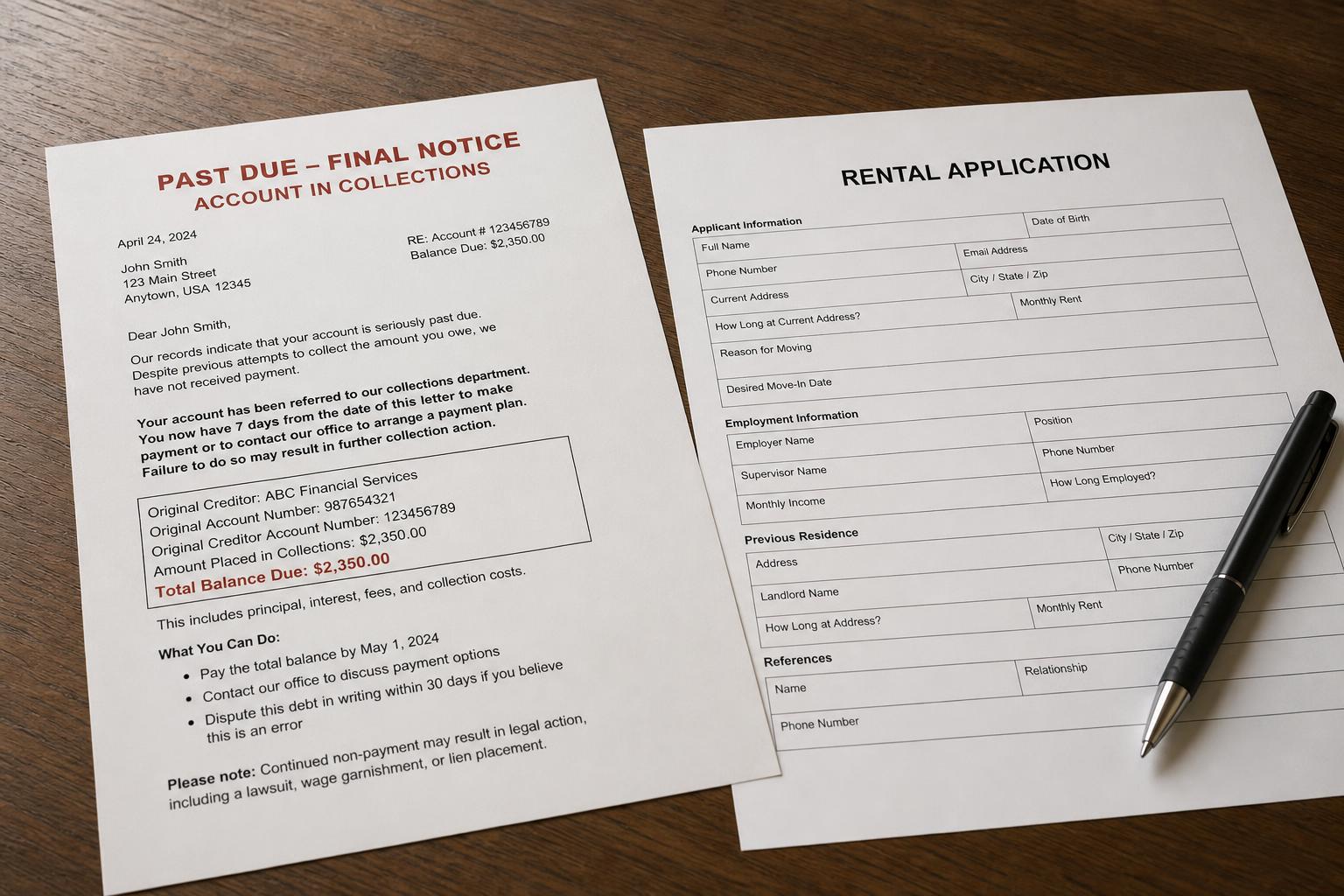

What if the collection is from a previous apartment?

A collection tied to a former landlord — unpaid rent, damages, or a broken lease — is the one to take most seriously, because it speaks directly to the question a new landlord is asking. It may appear on your credit report and your tenant-screening report.

Address it head-on: confirm the amount is accurate (these are frequently disputed), and if it’s valid, consider settling it — getting the terms and the reporting outcome in writing first. Being able to show a former rent debt is resolved, with a brief explanation of what happened, can turn the single biggest objection into a non-issue.

Does a utility or cell-phone collection affect renting?

It can. A landlord reviewing your credit sees all collections, not just rental ones — and a utility or phone collection signals the same thing they worry about: unpaid recurring bills. The good news is these tend to be weighed as a yellow flag rather than a dealbreaker, especially if they’re small, old, or paid. Treat them like any other collection: confirm the amount is accurate, dispute it if it isn’t, and be ready to explain it briefly. A resolved or explained utility collection rarely sinks an otherwise-strong application.

How to explain a collection to a landlord

A short, honest note can defuse a collection before it becomes a question. Keep it to a few sentences: name what happened (a job loss, a medical bill, a billing dispute), say what’s changed (steady income now, the balance resolved or being disputed), and attach proof — pay stubs, a payment receipt, or a reference. Lead with it rather than hoping the landlord won’t notice; volunteering the context reads as responsibility, and it lets you frame the collection instead of letting the report speak for you.

Watch out for debt-collection scams

People with collections are targets for fake-debt-collector scams. The FTC warns to be cautious when a “collector”:

Signs a debt collector may be fake

The bottom line on renting with collections

A collection narrows your options, but it rarely closes the door. The renters who get approved are the ones who check their reports first, fix what’s wrong, and walk in with income, references, and a straight answer ready.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

See what’s really on your report — free

A free 15-minute review shows what collections are reporting, what may be inaccurate or disputable, and how to apply with confidence — before your next rental application.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.