Medical debt & credit

Do Medical Bills Affect Your Credit Score? The Rules Have Changed

Medical debt is treated differently from other debt — and the rules shifted sharply in consumers’ favor. Here’s what actually lands on your credit report today, and what doesn’t.

Quick answer

A medical bill doesn’t go on your credit report — but an unpaid bill sent to collections can. Even then, the national credit bureaus now leave off paid medical collections and those under $500, and they wait about a year before an unpaid medical collection can appear at all.

So a recent or small medical bill usually isn’t hurting your score — and if something is showing that shouldn’t be, it may be disputable. Because the rules keep changing, it’s worth confirming what’s actually on your report before you assume the worst or pay the wrong thing.

Medical bills in collections? A free 15-minute review shows what’s actually reporting — and what may be inaccurate or disputable.

No credit card · phone optional · no obligation.

Does a medical bill go on your credit report?

No. Your credit report tracks credit accounts — loans, cards, and the like — not the bills your doctor or hospital sends. A medical bill only becomes a credit-report issue if it goes unpaid long enough that the provider hands it to a collection agency, and that agency reports it. Until that happens, the bill itself is invisible to your score.

When does medical debt actually hit your credit?

Only as a collection — and now only after a waiting period. The national credit bureaus give you about a year before an unpaid medical collection can appear (up from the old 180 days). That window exists precisely because medical billing is messy: it gives you time to sort out insurance, catch errors, and set up payment before anything touches your credit.

What changed: the credit-bureau medical-debt rules

The three nationwide bureaus — Equifax, Experian, and TransUnion — made several voluntary changes that work in your favor:

- Paid medical collections are removed from credit reports.

- Medical collections under $500 are removed (and no longer added).

- Unpaid medical collections wait about a year before they can appear.

Together, these keep most everyday medical debt off your credit report entirely.

What about the CFPB medical-debt rule?

You may have seen headlines about a federal rule removing medical debt from credit reports. A Consumer Financial Protection Bureau (CFPB) rule to do that was finalized in early 2025 but vacated in court later that year, so it is not currently in effect. Separately, a number of states have passed their own laws limiting medical debt on credit reports. The practical takeaway: this area keeps changing and varies by where you live — verify what’s currently true before you act.

Do newer credit scores treat medical debt differently?

Yes. Newer scoring models — like FICO 9 and VantageScore 3.0 and 4.0 — weigh medical collections less heavily than other collections, and ignore paid collections. But many lenders still use older models (such as FICO 8) where a medical collection can count more. Which model a given lender uses is out of your control, which is one more reason to keep your report clean of items that shouldn’t be there.

How much can a medical collection lower your score?

There’s no single number. The impact depends on the scoring model, how recent the collection is, and the rest of your profile — a collection on an otherwise-clean file can hurt more than one on a file that already has issues. Rather than guess at a point figure, it’s more useful to confirm whether the collection should be reporting at all.

How long does medical debt stay on your credit report?

A reporting medical collection can remain for up to seven years from the original delinquency date — but the bureau rules often remove it sooner. Once you pay it, it should come off; if it’s under $500, it shouldn’t be there at all. If a paid or small medical collection is still showing past those rules, that’s an error you can dispute.

What to do if medical debt is hurting your credit

Work the problem in order:

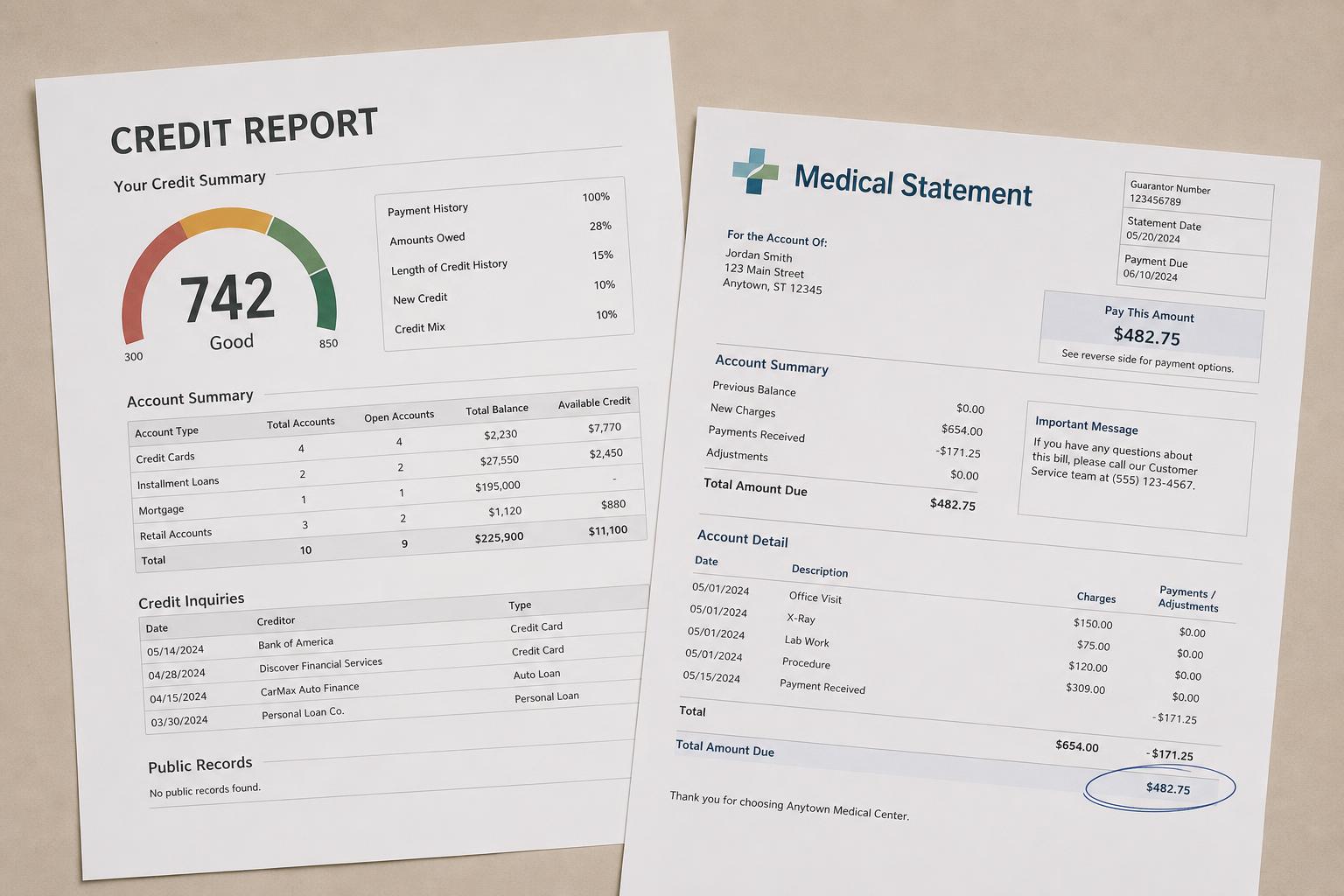

- Get your credit reports and find any medical collections.

- Check accuracy — against your insurance explanation of benefits and the provider’s itemized bill.

- Dispute errors under the Fair Credit Reporting Act (FCRA).

- Confirm the current rules apply — paid, under $500, or within the waiting window.

A free 15-minute medical-debt review helps you see what’s actually reporting and what may not belong — before you pay or settle anything.

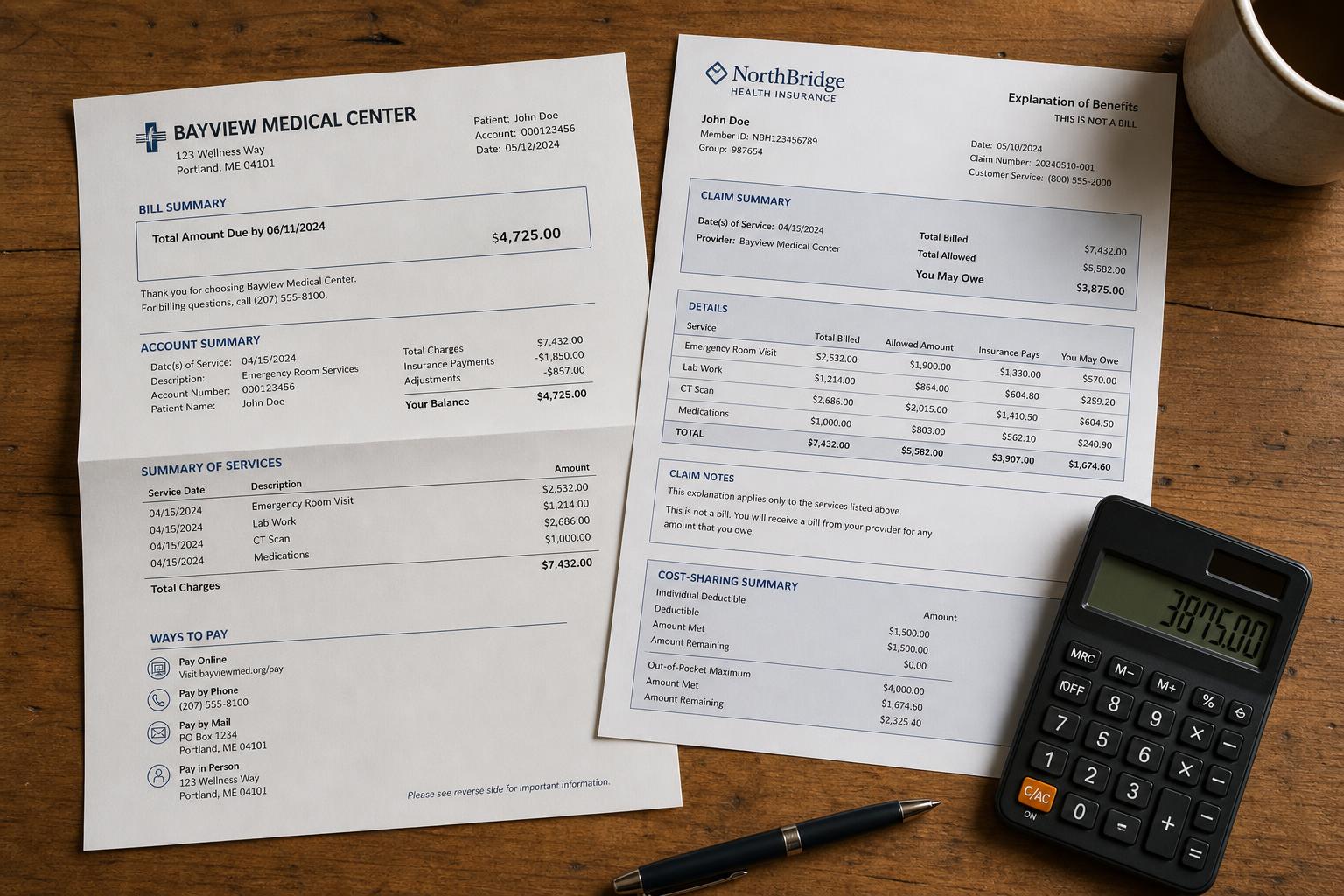

What if my insurance was supposed to pay the bill?

This is one of the most common — and most fixable — medical-debt problems. Bills end up with you (or in collections) because a claim was denied, miscoded, or never submitted. Before you pay anything, compare the provider’s bill against your insurance explanation of benefits (EOB). If the EOB shows the insurer should have covered it, contact the provider and insurer to get the claim reprocessed. A collection for a bill your insurance owed may be both wrong and disputable under the Fair Credit Reporting Act.

Does medical debt affect getting a mortgage or an apartment?

It can, indirectly. Most landlords and many mortgage lenders pull credit, so a reporting medical collection could surface — but the bureaus’ rules (paid and under-$500 collections removed, a one-year wait) keep a lot of medical debt off the report entirely, and newer mortgage scoring weighs it less. The practical move before a big application is to confirm what’s actually reporting across all three bureaus and dispute anything that shouldn’t be there, so an old medical bill doesn’t surprise you at the worst moment.

Medical bills and credit: do’s and don’ts

Do

Don’t

The bottom line

Medical debt is treated more gently than it used to be: bills aren’t on your report, small and paid collections are off it, and unpaid ones wait a year. The smartest move is to check what’s actually reporting and dispute anything that shouldn’t be there — not to panic-pay.

Key takeaways

Before you pay or settle a medical bill, confirm what’s actually reporting. A free 15-minute review shows what may be inaccurate, outdated, or disputable — before you act. See the free medical-debt review →

See what medical debt is really on your report — free

A free 15-minute review helps you spot what’s actually reporting, what may be inaccurate or shouldn’t be there, and what to do before you pay or settle.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.