Before you pay

How to Negotiate or Lower a Medical Bill Before It Hurts You

A medical bill isn’t always the final word — the price is often negotiable, and the bill itself is frequently wrong. Here’s how to lower what you owe, ideally before it ever reaches a collector or your credit report.

Quick answer

Medical bills are often negotiable, and they’re frequently inaccurate. Start by getting an itemized bill and checking it against your insurance explanation of benefits; ask about financial assistance or charity care; request a prompt-pay, cash, or self-pay discount; and set up an interest-free payment plan.

Do this before the bill goes to collections, while you’re still dealing with the provider — that’s when you have the most leverage and the most options. Verifying the bill first means you never overpay for an error.

Medical bills in collections? A free 15-minute review shows what’s actually reporting — and what may be inaccurate or disputable.

No credit card · phone optional · no obligation.

Are medical bills really negotiable?

Often, yes — far more than most people assume. Hospitals and providers regularly accept less than the billed amount, offer discounts, and set up payment plans, because a partial payment now beats sending the account to collections later. The billed price is frequently a starting point, not a fixed one, especially for the uninsured or self-pay. The key is to engage early and ask — the worst answer is usually “no.”

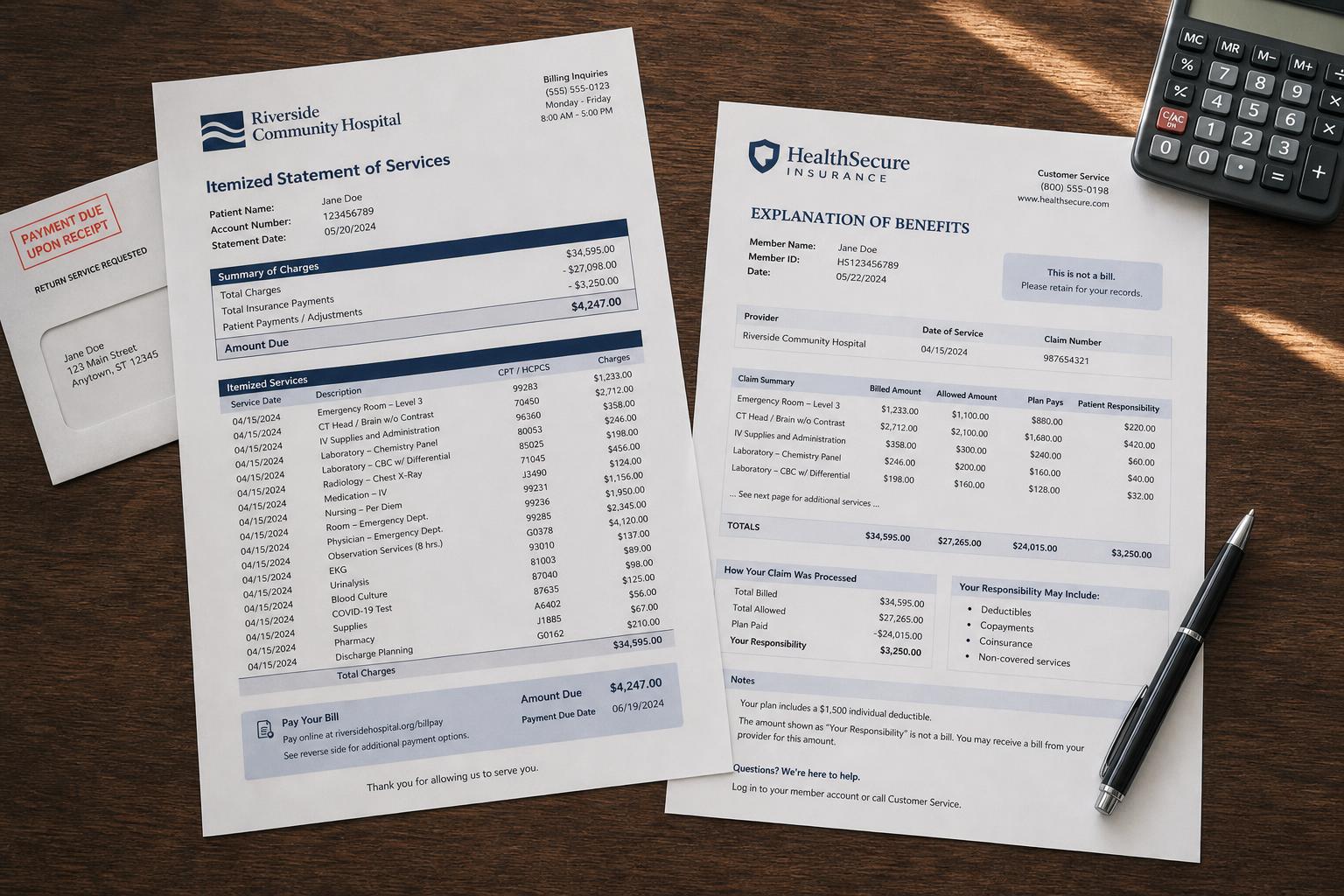

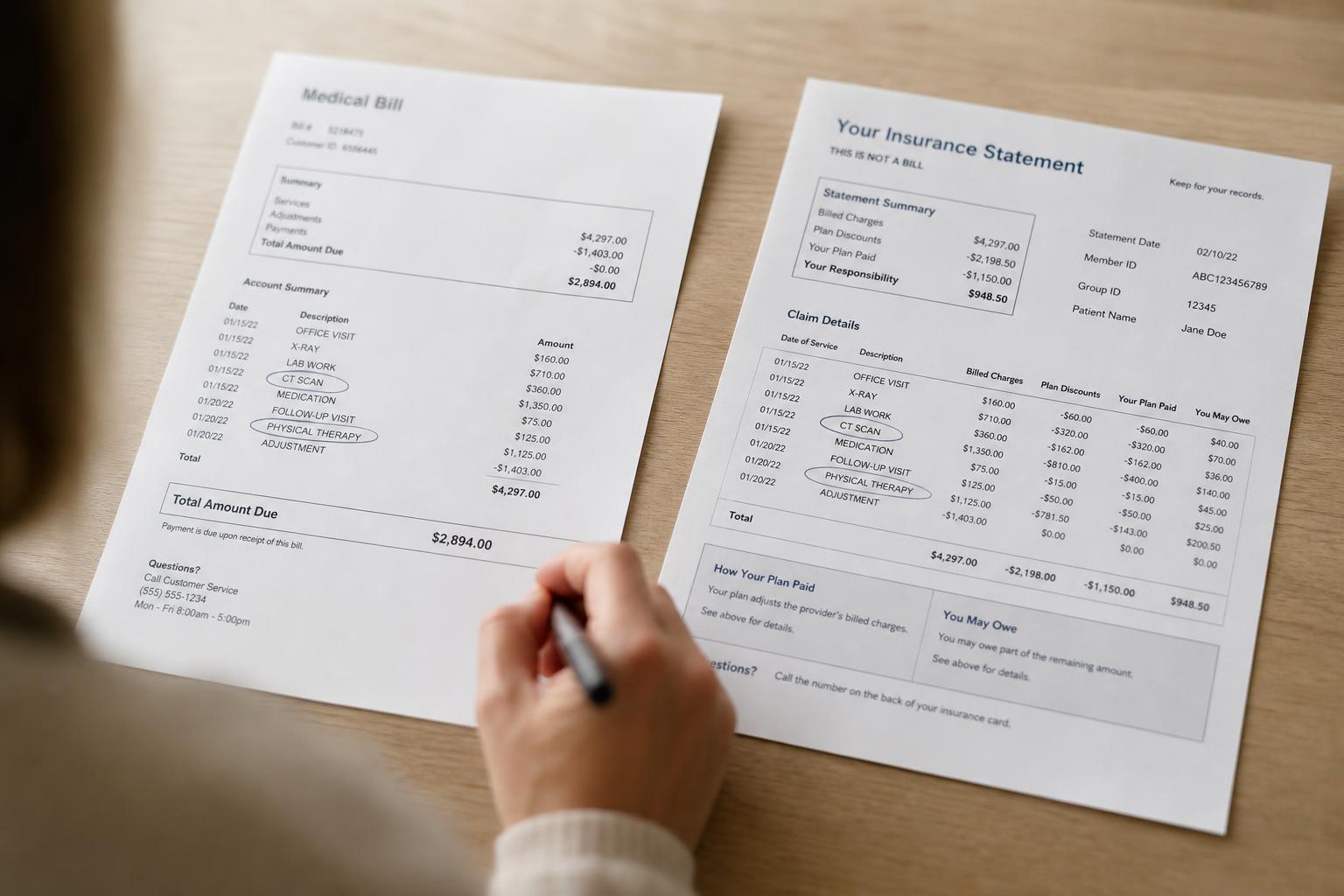

Step 1: Get an itemized bill and check it for errors

Always request a fully itemized bill — a line-by-line breakdown of every charge, not just a total. Then read it. Common, costly errors include:

- Duplicate charges for the same service

- Charges for services or medications you never received

- Incorrect billing or procedure codes (“upcoding” to a pricier service)

- Wrong quantities or days

Catching a single billing error can lower the total before you negotiate anything. You have the right to an itemized statement — ask for it in writing.

Step 2: Compare the bill against your insurance EOB

If you’re insured, line the bill up against your explanation of benefits (EOB) — the statement from your insurer showing what they paid and what you owe. Mismatches are common: a claim that wasn’t submitted, an in-network service billed as out-of-network, or a balance the insurer should have covered. If the bill and EOB don’t agree, the problem may be a billing or claims error, not money you actually owe.

If they don’t match

Contact both the provider’s billing office and your insurer. Sometimes the fix is simply resubmitting a claim — and the “balance” disappears.

Step 3: Ask about financial assistance or charity care

Many hospitals — and nonprofit hospitals in particular — offer financial assistance or charity care programs that reduce or eliminate bills for patients under certain income levels. Under federal rules, nonprofit hospitals are generally required to have a written financial assistance policy and to make it available. You often have to apply, and eligibility is usually income-based, so ask the billing office directly what programs exist and request the application. This is one of the most overlooked ways to lower a large hospital bill.

Step 4: Ask for a prompt-pay, cash, or self-pay discount

If you can pay some or all of the bill reasonably soon, ask whether there’s a prompt-pay discount or a self-pay/cash rate. Providers often discount for quick payment because it saves them collection costs. For the uninsured, the self-pay rate is frequently far below the “list” price. Always ask what the cash price would be — it can be a substantial reduction.

Step 5: Set up an interest-free payment plan

If you can’t pay at once, ask the provider for a payment plan. Many hospitals offer interest-free installment plans directly, which keeps the debt with the provider and out of collections. Agree only to a monthly amount you can sustain, and get the terms in writing. A plan you can actually keep is far better than a larger one you’ll default on.

Can you negotiate a lump-sum settlement?

Sometimes a provider or collector will accept a reduced lump sum to settle the balance. If you go this route, get the agreement — the amount and that it settles the account in full — in writing before you pay, and keep proof of payment. Be cautious: don’t commit to a lump sum you can’t actually cover, and understand that settling is a negotiation about the bill, not a guaranteed change to anything reported. Confirm in writing how the account will be treated once paid.

Why negotiate before it goes to collections?

Your leverage is highest while the bill is still with the original provider. Once it’s sold or assigned to a collection agency, you’re dealing with a third party, the math changes, and a collection can affect your credit report (subject to the medical-collection rules). Addressing the bill early — itemize, verify insurance, ask for assistance and discounts, set up a plan — keeps you in the stronger position and can keep the debt off your report entirely.

What if the bill is already in collections?

You still have options. First, request validation and verify the debt is accurate and yours — the same billing and insurance errors can ride along into collections. Then you can negotiate with the collector, set up a plan, or settle, getting any agreement in writing. And remember the medical-collection credit rules: paid medical collections are removed, and small or recent ones may not be eligible to report at all. We cover that in How to Remove Medical Collections and a free review.

Negotiating a medical bill

Preparation and politeness lower bills; panic and silence don’t.

Do

Don’t

Watch out when paying medical bills

Some “solutions” cost more than the bill. Be careful with:

Red flags

The bottom line on lowering a medical bill

A medical bill is a starting point, not a verdict. Itemize it, check it against your insurance, ask about charity care and discounts, and set up a manageable plan — before it reaches a collector. Verifying first means you only pay what you actually owe, and acting early can keep the bill off your credit report altogether.

Key takeaways

Before you pay or settle a medical bill, confirm what’s actually reporting. A free 15-minute review shows what may be inaccurate, outdated, or disputable — before you act. See the free medical-debt review →

Make sure you only pay what you actually owe

A free 15-minute review helps you see what’s on your credit report and what medical items may be inaccurate or disputable — so a bill never costs you more than it should.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.