Medical collections

A Collector Is Calling About a Medical Bill: Your Rights

A medical bill in collections is stressful — but you have real, enforceable rights, and medical bills are unusually prone to errors. Here’s what a collector must do, what they can’t, and why you should verify before you pay.

Quick answer

If a debt collector contacts you about a medical bill, the Fair Debt Collection Practices Act (FDCPA) protects you: you’re entitled to a written validation notice, the right to dispute the debt, the ability to limit how and when they contact you, and freedom from harassment, threats, and false statements.

Medical bills deserve extra scrutiny — billing and insurance errors are common, and recent changes to how the credit bureaus treat medical collections affect whether the debt can even appear on your report. Verify before you pay anything.

Do debt collectors have to follow rules?

Yes. The Fair Debt Collection Practices Act (FDCPA) is a federal law governing how third-party debt collectors can behave, and the Consumer Financial Protection Bureau (CFPB) enforces it. It applies to medical debt that’s been turned over to a collection agency. The law gives you specific rights and bars a long list of abusive tactics — and a collector who violates it can be liable to you.

Knowing the rules changes the dynamic. A collector counting on confusion behaves differently with someone who calmly asks for validation and references their FDCPA rights.

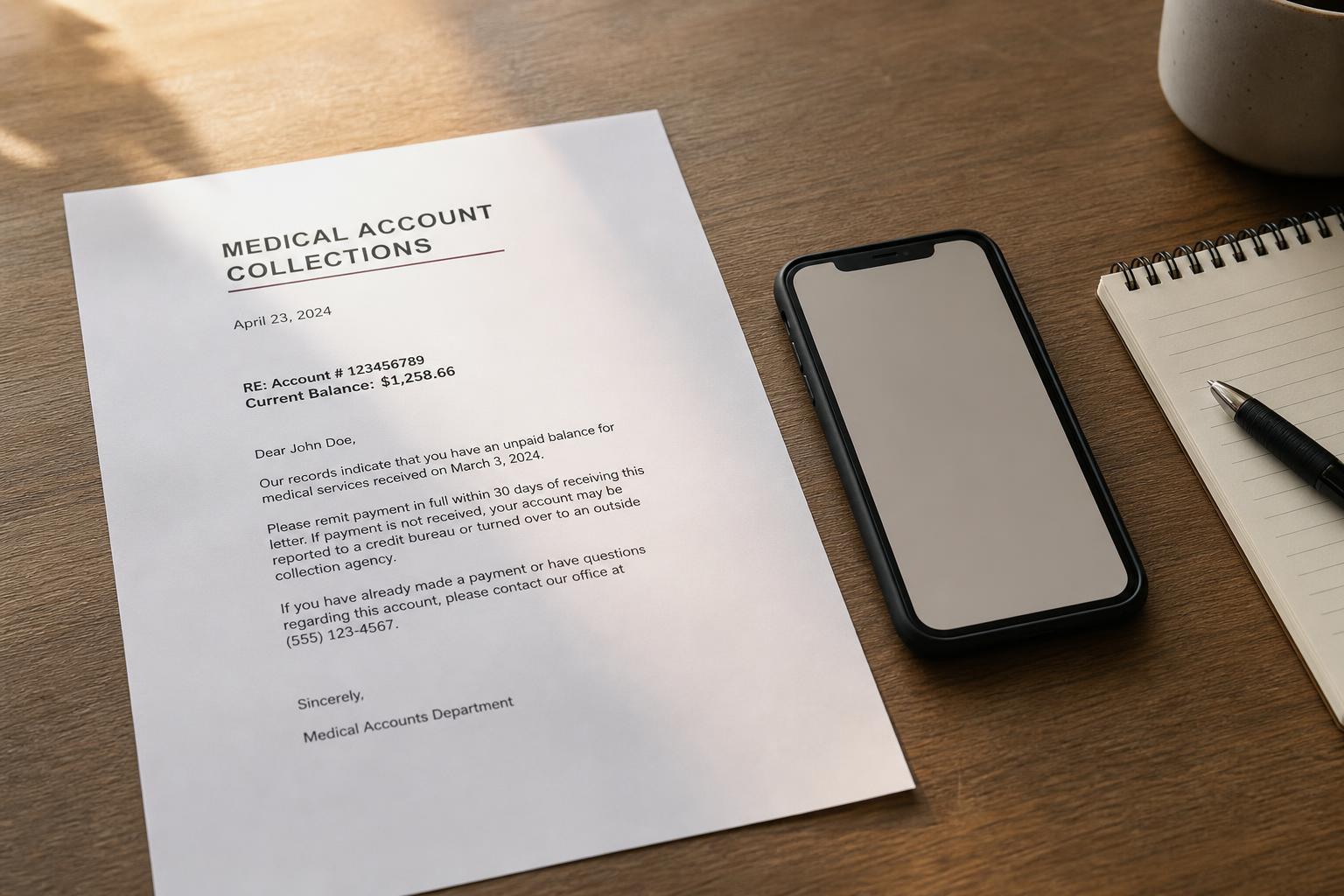

What is a validation notice, and what must it include?

Shortly after first contacting you, a collector generally must send a validation notice in writing. It should identify the amount of the debt, the name of the creditor you owe, and information on how to dispute it. This notice is your anchor: it tells you who’s collecting, for what, and on whose behalf — the facts you need to check whether the debt is accurate and actually yours.

If you don’t get one

If a collector contacts you without sending written validation, you can request it. Don’t pay or commit to anything based on a phone call alone — get it in writing first.

How do you dispute a medical debt with a collector?

You have the right to dispute. If you send a written dispute — ideally within 30 days of the validation notice — the collector generally must pause collection until they verify the debt and send you proof. For medical bills, a dispute is often well-founded: the amount may be wrong, insurance may not have been applied, or the debt may not be yours.

Put it in writing and keep a copy. Ask them to verify the debt and provide documentation. If they can’t validate it, they generally must stop collecting and shouldn’t continue reporting it as owed.

What are debt collectors not allowed to do?

The FDCPA prohibits a wide range of conduct. Collectors generally may not:

- Harass, threaten, or use abusive language

- Call you at unreasonable times (typically before 8 a.m. or after 9 p.m.)

- Contact you at work if you’ve told them you can’t take calls there

- Make false statements — about the amount, about being attorneys or government, or about consequences

- Threaten arrest or legal action they don’t intend or can’t take

- Discuss your debt with third parties like family or your employer

If a collector does these things, document it — dates, times, what was said — and you can report them to the CFPB and your state attorney general.

How do you stop or limit collector contact?

You can tell a collector, in writing, to stop contacting you — after which they may only confirm there will be no further contact or notify you of a specific action like a lawsuit. You can also specify limits, like no calls at work. Newer rules also address contact by text and email and let you opt out of specific channels.

One caution: stopping contact doesn’t make the debt go away or stop it from being reported — it just ends the calls. If the debt is legitimate, you’ll still want to verify and address it.

Why are medical bills especially worth disputing?

Medical billing is complex, and errors are common — duplicate charges, services you didn’t receive, incorrect billing codes, or a balance that should have been covered by insurance. Sometimes a bill lands in collections because a claim was never properly submitted, or because of a coordination-of-benefits mixup. Before paying a medical collection, it’s genuinely worth confirming the underlying bill is right and that your insurance was applied correctly. What may be inaccurate, you have the right to dispute.

How do the medical-collection credit rules affect this?

Separate from the FDCPA, the national credit bureaus (Equifax, Experian, and TransUnion) made voluntary changes to how medical collections appear on credit reports: paid medical collections are removed, there’s a waiting period (about a year) before an unpaid medical collection can appear, and medical collections under a certain dollar threshold (around $500) are no longer included. A federal CFPB rule that would have gone further was finalized in early 2025 but later vacated, so it is not currently in effect. Rules in this area have been shifting and can vary — verify what’s reporting on your own file rather than assuming.

Should you pay, dispute, or wait?

Don’t default to paying just to make the calls stop. First confirm the debt is yours and the amount is right; check whether insurance should have covered it; and see whether it’s even reporting given the medical-collection rules. If it’s inaccurate, dispute it. If it’s valid, you can negotiate the bill or set up a plan — ideally after verifying. Paying an unverified medical collection can mean paying something you didn’t owe, or that should have been covered.

Dealing with a medical-debt collector

Calm and documented beats rushed and verbal every time.

Do

Don’t

Fake and abusive collector red flags

Medical debt attracts scammers and rule-breakers. Be on guard for:

Red flags

The bottom line on medical collections

A medical bill in collections doesn’t strip you of rights — it triggers them. Get validation, scrutinize the bill for the errors that plague medical billing, dispute what’s wrong, and understand the medical-collection credit rules before you decide to pay. The collector is counting on urgency; your advantage is verification.

Key takeaways

Before you pay or settle a medical bill, confirm what’s actually reporting. A free 15-minute review shows what may be inaccurate, outdated, or disputable — before you act. See the free medical-debt review →

Verify what a collector is reporting — free

A free 15-minute review shows what medical collections are on your report and what may be inaccurate, unpaid in error, or no longer eligible to report — before you pay a cent.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.