Before you sign

Rent-to-Own Homes With Bad Credit: How They Work and the Catch

Rent-to-own sounds like a way around bad credit — rent now, buy later. But the credit problem is usually deferred, not erased. Here’s how these deals really work and what to check before you commit a dime.

Quick answer

Rent-to-own (a lease-option or lease-purchase) lets you rent a home now with the chance to buy it later, sometimes with part of your rent credited toward the purchase. But in most deals you still have to qualify for a mortgage when the option period ends — so bad credit doesn’t disappear; it’s deferred to that deadline.

Option fees and above-market “rent credits” are often nonrefundable if you can’t buy. That makes the years in between valuable: the smartest use of a rent-to-own is to spend that time understanding and improving what’s on your credit so you can actually qualify at the finish line.

What is rent-to-own, and how does it work?

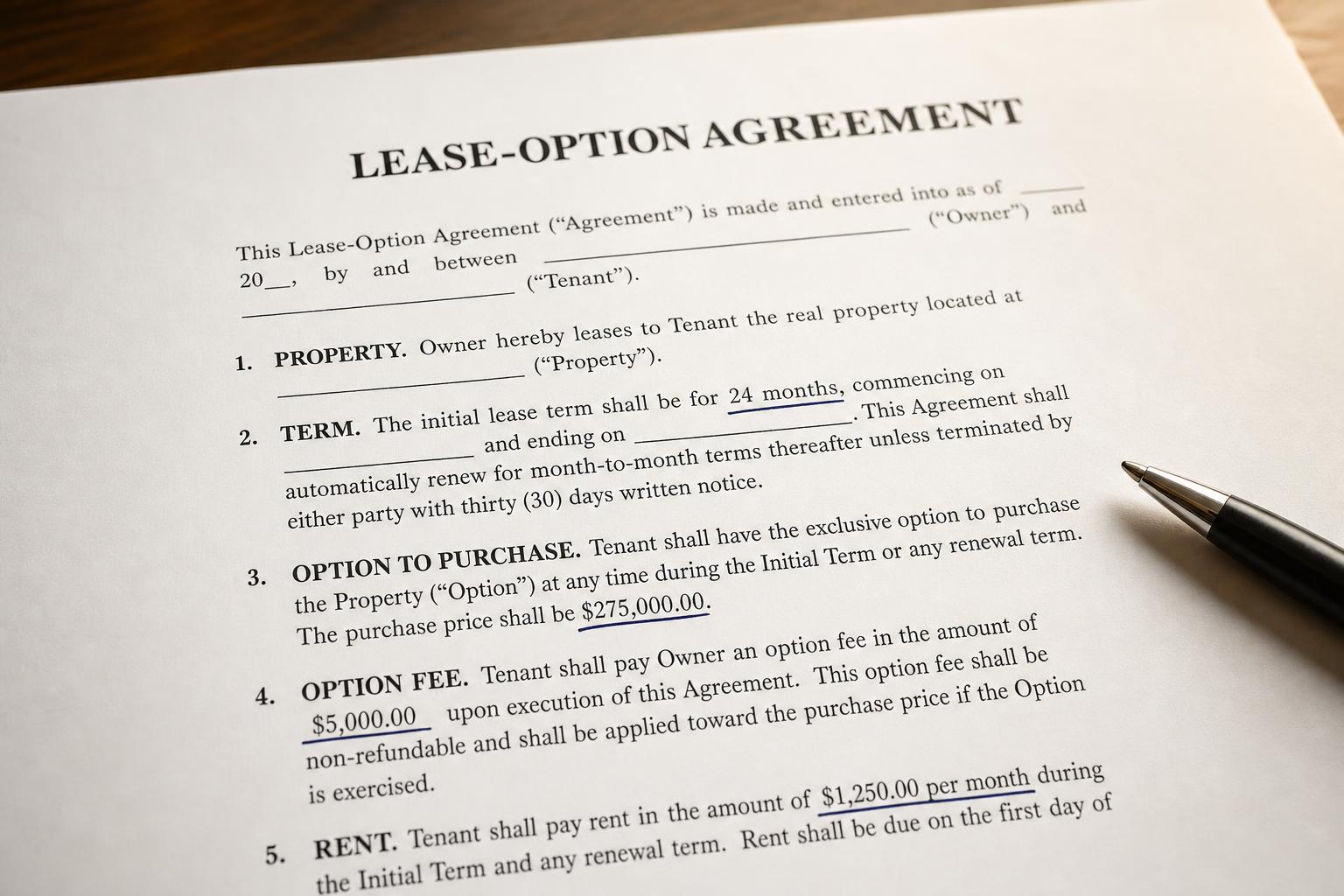

Rent-to-own is an umbrella term for two related arrangements. In a lease-option, you sign a lease plus a separate option giving you the right — but not the obligation — to buy the home at a set price within a set period. In a lease-purchase, you commit to buying at the end. You typically pay an upfront option fee and sometimes a rent premium, with part of it credited toward the eventual purchase.

The appeal is obvious if your credit isn’t mortgage-ready today: you lock in a home and a price while you work toward qualifying. The risk is in the details of how, and whether, that purchase actually happens.

How does rent-to-own work with bad credit?

Here’s the part that surprises people: in most rent-to-own deals, you still need to qualify for a mortgage to complete the purchase. The landlord-seller isn’t usually financing the home long-term — they’re renting it to you until you can get your own loan. So if your credit isn’t ready by the deadline, you may not be able to buy, no matter how faithfully you paid rent.

That doesn’t make rent-to-own useless — it makes the credit timeline the whole ballgame. The arrangement only pays off if you use the lease period to get genuinely mortgage-ready.

What are the option fee and rent premium — and are they refundable?

The option fee is an upfront payment (often a few percent of the price) for the right to buy. A rent premium or “rent credit” is extra monthly rent, part of which may count toward the purchase. In most contracts, if you don’t buy — for any reason, including not qualifying for a loan — you forfeit the option fee and the accumulated credits.

Why this matters

Because these payments are at risk, a rent-to-own is only a good deal if you’re realistically on track to qualify. Otherwise you may pay above-market rent for years and walk away with nothing to show for the premium.

The big catch: you usually still have to qualify for a loan

It bears repeating because it’s the most common misunderstanding. A rent-to-own does not replace a mortgage; it postpones one. When the option period ends, you generally apply for a home loan like any buyer — with your credit, income, and debt all under the microscope. If anything on your report still blocks approval, the deal can collapse at the worst possible moment.

So the practical question isn’t “can I find a rent-to-own?” but “will my credit be mortgage-ready by the deadline?” That’s worth answering honestly before you sign.

What happens if you can’t buy at the end?

In a lease-option, you typically lose the option fee and any rent credits, and you move out — the purchase simply doesn’t happen. In a lease-purchase, where you committed to buy, failing to complete can expose you to greater liability, since you agreed to purchase rather than merely holding an option. Either way, the downside lands on you, which is why the type of contract and the exit terms matter enormously.

Lease-option vs. lease-purchase: what’s the difference?

The distinction is about obligation. A lease-option gives you the right to buy but lets you walk away (forfeiting fees). A lease-purchase obligates you to buy — which can be riskier if your financing falls through. If you’re uncertain whether your credit will be ready, a lease-option generally carries less downside than a binding lease-purchase. Read which one you’re actually being offered; the names are sometimes used loosely.

Is rent-to-own a good idea with bad credit?

It can be — if three things are true: the contract terms are fair, you can comfortably afford the rent and premium, and you have a realistic plan to become mortgage-ready before the deadline. If any of those is shaky, you may be paying a premium for an option you can’t exercise. For many people, simply renting affordably while addressing their credit — then buying with a conventional or FHA loan later — is lower-risk than a rent-to-own.

What should you check before signing a rent-to-own contract?

Protect yourself before any money changes hands:

- Confirm the seller actually owns the home and that the mortgage is current — if they stop paying, the home can be foreclosed out from under you.

- Get the purchase price, option period, and credit terms in writing, and have the contract reviewed by a real estate attorney.

- Clarify who pays for repairs, taxes, and insurance during the lease.

- Ask how rent credits are tracked and what voids them (a late payment sometimes does).

- Record the option where your state allows, to protect your interest.

The Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) both caution that rent-to-own and lease-option deals can carry hidden risks — due diligence is essential.

Rent-to-own red flags and scams

These deals attract bad actors who target buyers with limited options. Walk away if you see:

Red flags before you pay

Doing rent-to-own the safer way

If you pursue a rent-to-own, treat it like the major financial commitment it is.

Do

Don’t

The bottom line on rent-to-own with bad credit

Rent-to-own can be a genuine bridge to ownership — but only if you’ll be mortgage-ready when the option comes due, and only if the contract is fair. Bad credit isn’t erased by these deals; it’s parked until the deadline. Treat the lease years as your window to address what’s on your report, and read every clause before you commit.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

Will your credit be ready when the option comes due?

A free 15-minute review shows what’s on your credit report today — and what may be affecting future mortgage approval — so a rent-to-own deadline doesn’t catch you off guard.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.