After a denial

Can You Appeal an Apartment Denial or Reapply?

A rental denial usually isn’t the end of the conversation. Here’s how to find out what triggered it, ask a landlord to reconsider, and decide when reapplying actually makes sense.

Quick answer

Often, yes — though there’s rarely a formal “appeals” process. If you were denied based on a report, the landlord must send an adverse action notice naming the screening company, which is your starting point. From there you can ask the landlord to reconsider with new information, dispute an inaccurate report, or reapply once you’ve addressed the cause.

What rarely works is reapplying blindly: without changing what triggered the denial, you’ll usually get the same answer and lose another application fee. Find the reason first, then act on it.

Can you appeal an apartment denial?

There usually isn’t a formal appeals board, but there is almost always room to ask a landlord to reconsider — especially independent landlords and smaller managers who make decisions by hand. “Appealing” here means reopening the conversation with something new: information that addresses their concern, evidence the denial rested on an error, or an offer that lowers their risk. Whether they’ll budge depends on the landlord and the reason, but it costs little to ask politely and well-prepared.

Start with the adverse action notice

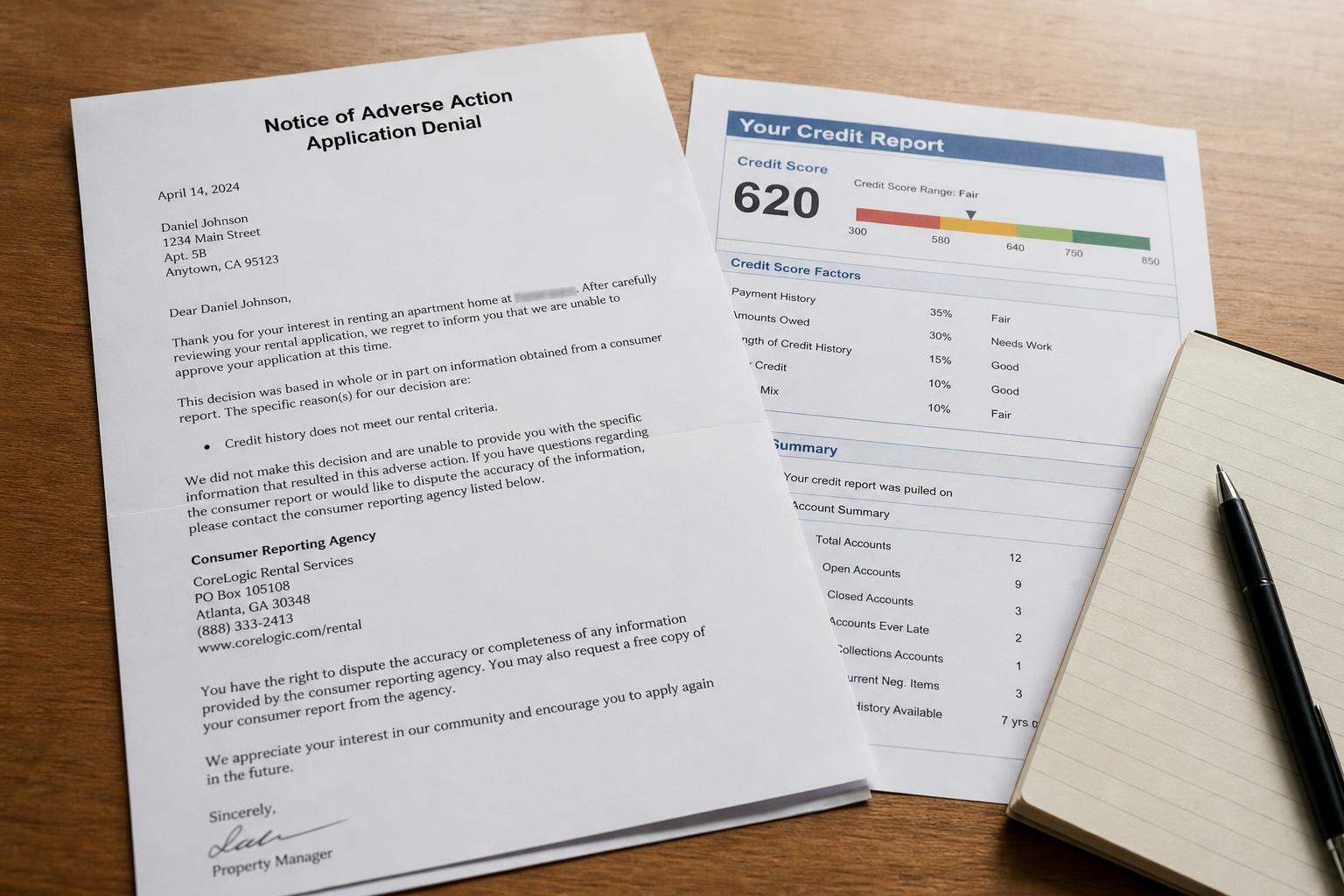

If your application was denied because of a consumer report, federal law (the FCRA) requires the landlord to give you an adverse action notice. It must identify the screening company that supplied the report and tell you that you can get a free copy and dispute inaccuracies. This notice is the single most useful thing you can get after a denial — it points you straight to the file that drove the decision.

If you didn’t receive one and you suspect a report was involved, you can ask the landlord for it. Without the notice, you’re guessing; with it, you know exactly where to look.

Ask the landlord exactly what triggered the denial

Politely ask which specific factor drove the decision — credit, income, rental history, an eviction record, or something else. Landlords aren’t always required to give granular detail, but many will, and the answer determines your next move. A denial over an inaccurate eviction record calls for a dispute; a denial over income calls for a co-signer or more documentation. You can’t fix what you can’t name.

How do you ask a landlord to reconsider?

Come back with something that changes the math, not just a request.

Offer to reduce their risk

A co-signer or guarantor, a larger security deposit, or a few months’ rent up front can move a borderline decision. You’re giving the landlord a concrete reason to feel comfortable.

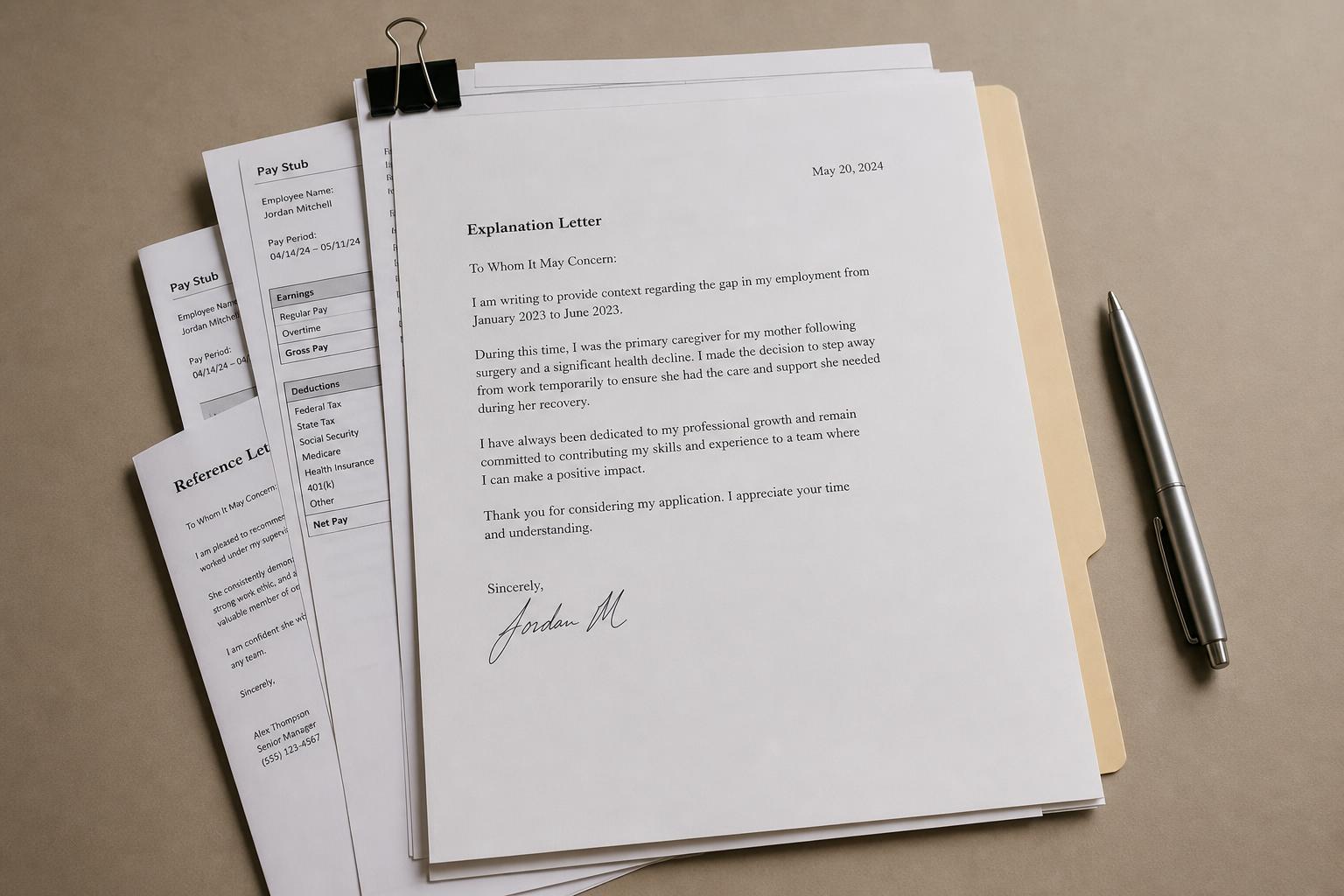

Explain the context briefly

A short, honest note explaining a past problem — a medical event, a job loss, since resolved — plus proof you’ve been reliable since, helps a human landlord see beyond a single data point.

Bring stronger proof

Additional pay stubs, an employer letter, or prior-landlord references can answer the specific worry behind the denial.

Dispute the report if the denial was based on an error

If the denial traces to something inaccurate — a collection that isn’t yours, a dismissed eviction reported as active, a mixed file — you have the right under the FCRA to dispute it with the screening company or credit bureau reporting it. They generally must investigate, typically within about 30 days, and correct or remove what they can’t verify. Once the record is corrected, you can ask the landlord to reconsider or apply again on accurate information.

When does it make sense to reapply?

Reapply when something has actually changed: you’ve corrected an error, added a co-signer, gathered better documentation, or paid down a balance the landlord flagged. Reapplying to the same landlord without any change usually yields the same result. Applying to a different, more flexible landlord can make sense immediately — especially one who weighs income and references rather than a rigid score cutoff.

How long should you wait to reapply?

There’s no fixed waiting period — the right timing is tied to the cause, not the calendar. If you’re disputing an error, wait until it’s corrected. If you’re strengthening the application, wait until you have the co-signer or documents in hand. Reapplying the same week with nothing new just burns fees. The goal is to reapply changed, not merely later.

Does reapplying or applying elsewhere hurt your credit?

It can leave inquiries. A rental application that pulls your credit may create a hard inquiry, which can have a small, temporary effect on your score; the denial itself isn’t recorded on your report. Applying to many places in a short window stacks up inquiries, which is one more reason to apply deliberately rather than blanketing the market. We cover this in more detail in Does an Apartment Denial Hurt Your Credit?

What about fair housing and reasonable accommodations?

If you believe a denial was based on a protected characteristic — race, disability, family status, national origin, and others under the Fair Housing Act — that’s a different path: you can contact the U.S. Department of Housing and Urban Development (HUD) or a local fair-housing agency. Renters with disabilities can also request reasonable accommodations in a landlord’s policies. These protections are about discrimination, not ordinary credit or income screening, but they matter if that’s what’s really going on.

Appealing and reapplying the right way

Treat a denial as a problem to diagnose, not a door that’s closed.

Do

Don’t

Watch out for these after a denial

People who’ve just been turned down are prime targets. Be cautious of:

Red flags

The bottom line on appealing a denial

A rental denial is usually the start of a fixable problem, not the end of your search. Use the adverse action notice to find the cause, come back to the landlord with something new, dispute anything inaccurate, and reapply only once you’ve genuinely changed the picture — to that landlord or a more flexible one.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

Find the real reason behind your denial — free

A free 15-minute review shows what’s on your credit report behind a rental denial — what may be inaccurate or disputable — so you can appeal or reapply with a plan, not a guess.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.