After a denial

Does Getting Denied for an Apartment Hurt Your Credit?

A rental denial stings — but does it actually damage your credit? Here’s what happens to your report when you apply and get turned down, and the right next move.

Quick answer

No — being denied for an apartment does not lower your credit score, and the denial itself isn’t recorded on your credit report. What can appear is an inquiry from the application, and whether that’s a soft or hard inquiry depends on how the landlord or screening company pulled your information.

The more useful question after a denial is why it happened — because the answer is usually on your credit or tenant-screening report, and often something you can address.

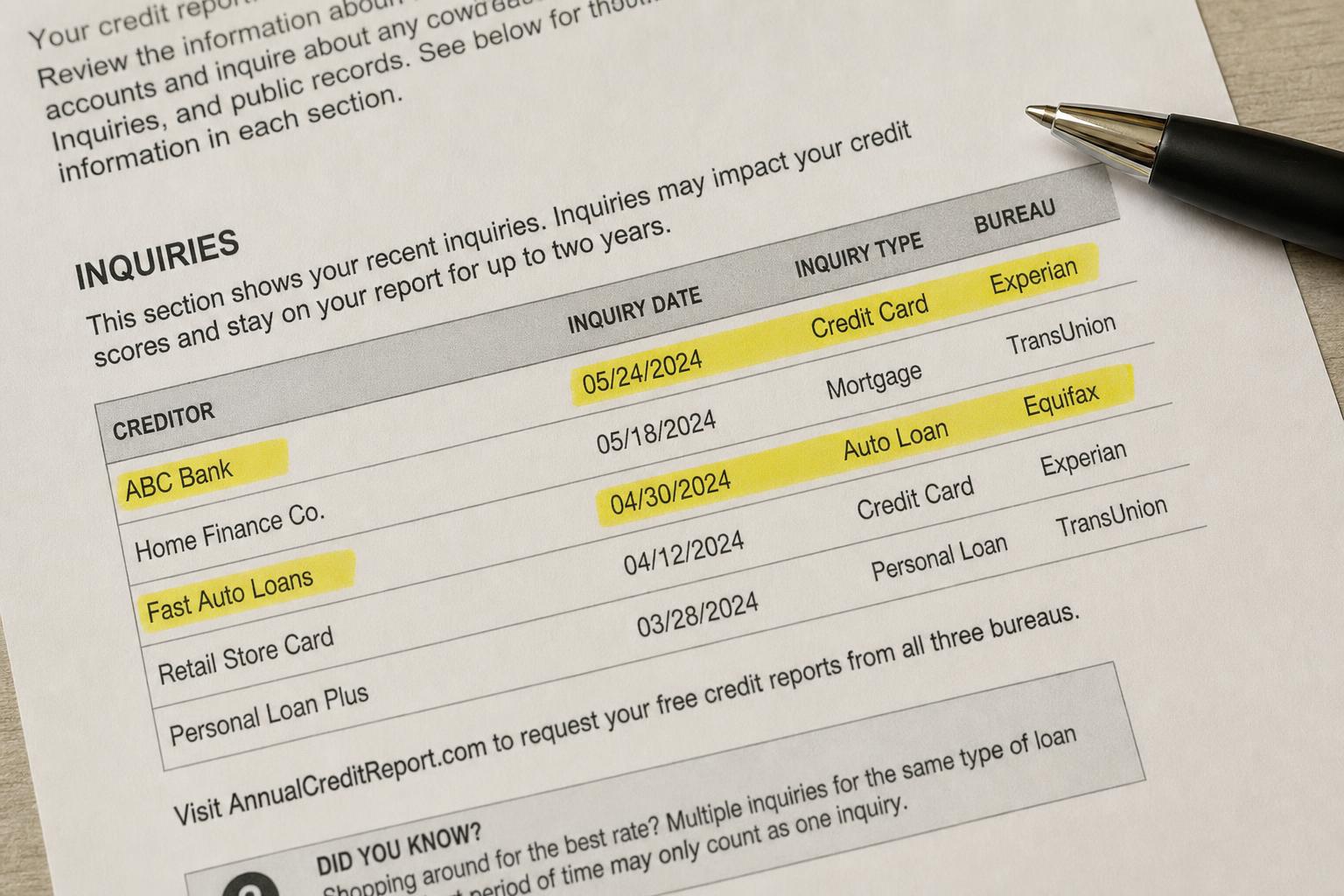

Does a rental application show up on your credit report?

Sometimes — as an inquiry, not as a “denial.” When you apply, the landlord or their screening company may check your credit, and that check can leave a record on your report. The key question is what kind of check it was.

The denial decision itself is never added to your credit report. Credit reports track accounts, balances, payment history, and inquiries — not whether a particular landlord said yes or no.

Soft inquiry vs. hard inquiry — what’s the difference?

This is the part that actually affects your score:

- A soft inquiry doesn’t affect your score at all. Many tenant-screening checks are soft pulls, and so is checking your own credit.

- A hard inquiry can lower your score by a small amount, usually for a few months. It stays visible on your report for about two years but typically only factors into your score for about one.

Whether a rental application triggers a soft or hard pull varies by landlord and screening company — it’s a fair question to ask before you apply.

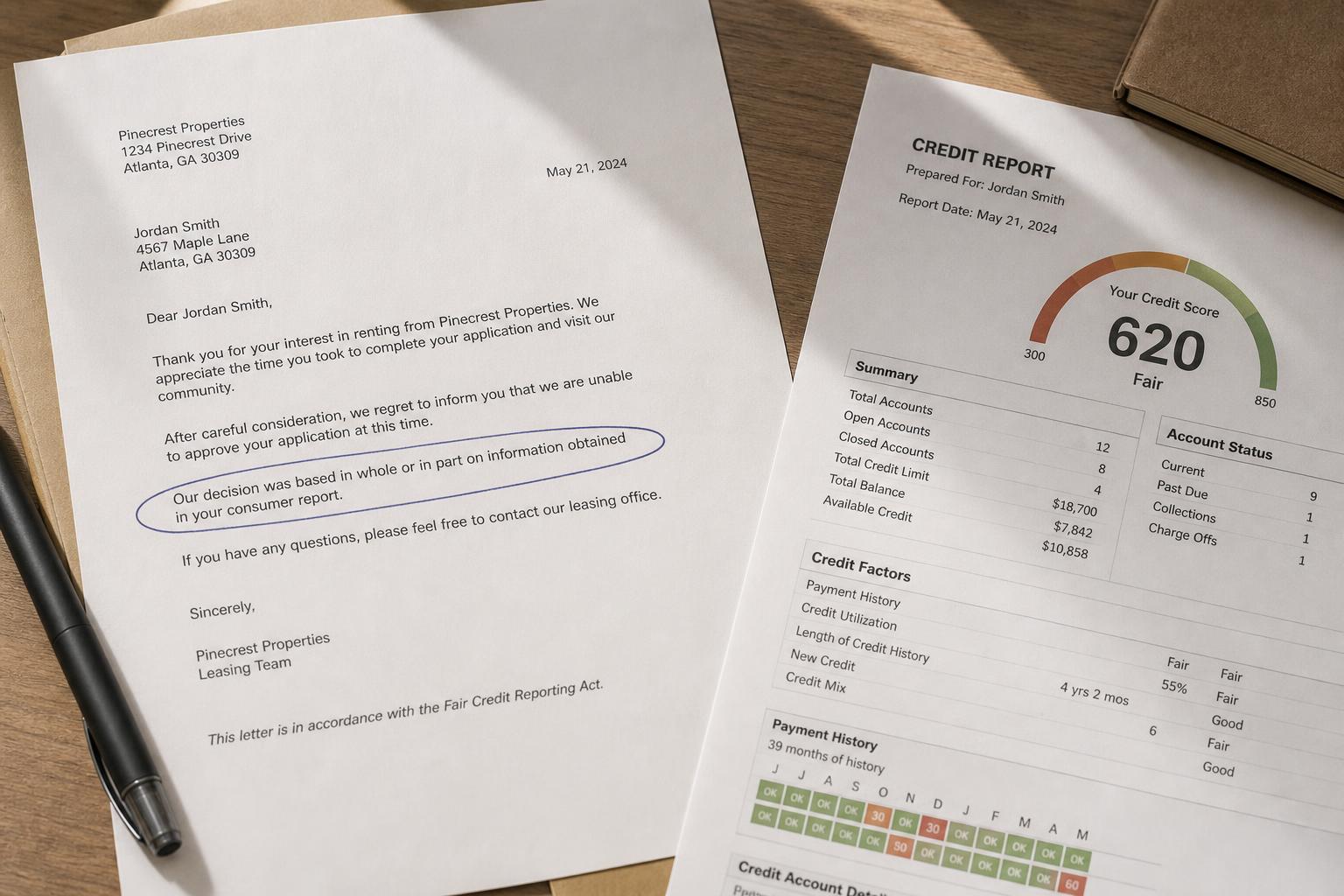

Does the denial itself go on your credit report?

No. There is no “denied for an apartment” line on a credit report. If a credit or tenant-screening report was used in the decision, though, the landlord is generally required under the Fair Credit Reporting Act (FCRA) to send you an adverse action notice — which names the company that supplied the report and tells you how to get a copy. That notice is a tool, not a mark against you.

Do multiple apartment applications hurt your credit?

They can add up — but only the hard pulls. If several landlords run hard inquiries in a short stretch, the small dings can stack. Soft-pull screenings don’t affect your score no matter how many you do. The practical takeaway: apply selectively, and where you can, ask whether the screening is a soft or hard pull before authorizing it.

So what actually shows up after a denial?

Usually nothing new. The denial added no negative mark; whatever led to it — a collection, a thin file, an eviction record, an error — was already on your report before you applied. That’s actually good news: it means the denial didn’t set you back, and the underlying cause is something you can look at and act on.

What to do after an apartment denial

Turn the “no” into information:

- Read the adverse action notice and note which company supplied the report.

- Request your report from that company — you’re entitled to a copy.

- Dispute any errors you find under the FCRA.

- Address what’s accurate and within your control, and explain it on your next application.

- Target flexible landlords like second chance apartments while you do.

A free 15-minute rental credit review helps you read what’s reporting and decide what to tackle first.

Can a landlord report you to the credit bureaus?

Usually not for routine rent — most landlords don’t report your monthly payments to the bureaus at all. But the picture changes if you owe money: unpaid rent, damages, or a broken lease can be sent to a collection agency, and that collection can appear on your credit report. A landlord might also win a court judgment for unpaid rent, which can surface in public records and on tenant-screening reports.

So a denial itself doesn’t touch your credit — but leaving a debt unresolved with a past landlord can. That’s a reason to settle old rent debts rather than ignore them.

Does checking your own credit before applying hurt your score?

No. Reviewing your own credit is a soft inquiry, which never affects your score — so there’s no downside to looking before you apply, and a real upside. You’ll see what a landlord will see, catch any errors in time to dispute them, and walk in able to explain anything that needs context. Checking first is one of the few moves that’s pure upside.

How many points does a hard inquiry cost?

Usually very few. A single hard inquiry typically shaves only a small number of points off your score, and the effect fades within a few months even though the inquiry stays visible for about two years. One application’s inquiry is rarely what makes or breaks you — the underlying report items matter far more. The time to be cautious is when several hard pulls stack up in a short window, which is why it’s worth asking whether a rental screening is a soft or hard pull before you authorize it.

How do you remove a hard inquiry you didn’t authorize?

If you spot a hard inquiry you never approved, you can challenge it. Unauthorized inquiries can signal an error — or even identity theft — and under the Fair Credit Reporting Act you can dispute them with the bureau and ask the company that pulled it to show your authorization. Legitimate inquiries you did authorize can’t simply be deleted and will age off on their own; but ones that aren’t yours don’t belong there. Reviewing your report after you apply is the best way to catch them early.

After a denial: do’s and don’ts

Do

Don’t

The bottom line

An apartment denial doesn’t hurt your credit score, and it leaves no “denial” mark on your report — at most a soft or hard inquiry from the application. The real value is in the reason: find it, fix what you can, and apply smarter next time.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

Find out why — not just that you were denied

A free 15-minute review shows what’s on your credit report behind the denial, what may be disputable, and a realistic next step before you apply again.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.