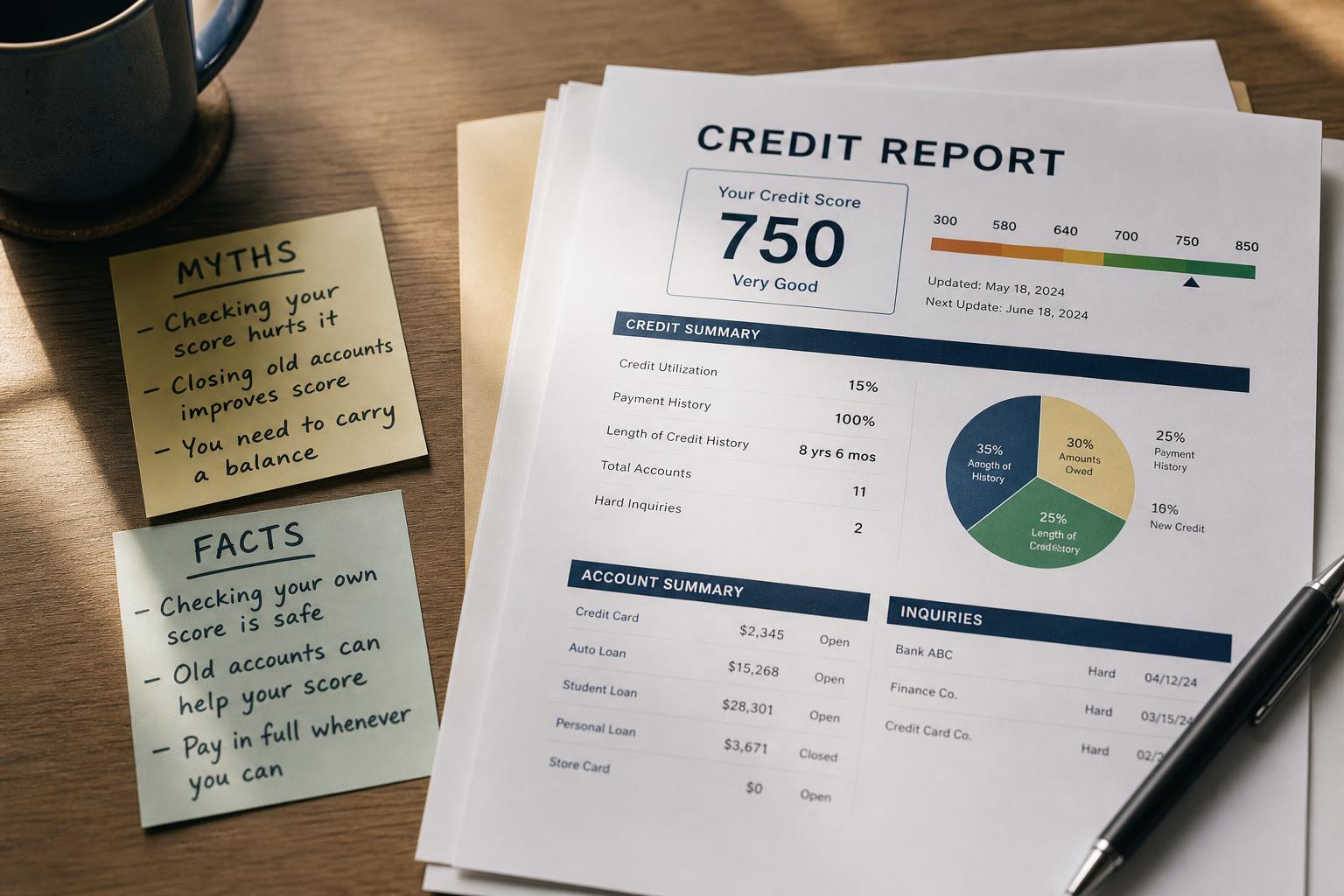

Common Credit Myths, Debunked

Credit is surrounded by confident-sounding advice that’s simply wrong — and some of it quietly costs people money. Let’s clear up the big ones.

Few topics attract as much bad advice as credit. Myths get passed around as fact, and acting on them can hold your score back or cost you in interest.

Here are the most common ones, and what’s actually true.

Myth: “Checking your own credit hurts your score”

False. Checking your own credit is a soft inquiry and never affects your score. Only hard inquiries — from applying for new credit — can, and only slightly. Check your own credit as often as you like.

Myth: “Carrying a balance helps your score”

False, and expensive. You do not need to carry a balance (and pay interest) to build credit. Paying your statement in full still reports positive history and on-time payments. Carrying a balance just costs you interest and can raise your utilization.

Myth: “Closing old cards helps your score”

Usually false. Closing a card removes its credit limit (which can raise your overall utilization) and, over time, can shorten your average account age. An old, no-fee card is often worth keeping open and lightly used, precisely because its age and limit help you.

Myth: “Your income is part of your credit score”

False. Income isn’t in your credit score at all — neither are your job, savings, age, or where you live. Lenders may consider income separately when you apply, but it doesn’t raise or lower the score itself.

Myth: “You have just one credit score”

False. You have many. There are multiple models (FICO, VantageScore) and versions, and three bureaus with slightly different data — so your score varies by source and by which one a lender pulls. That’s normal; focus on the underlying report, not one magic number.

Myth: “Paying a collection always removes it”

False. Paying a collection generally updates its status to “paid” but doesn’t automatically delete it from your report (medical collections follow gentler rules). And no legitimate service can erase accurate negative information — only genuine errors can be disputed off (here’s how disputes work).

Key takeaways

- Checking your own credit is a soft pull — it never hurts your score.

- You don’t need to carry a balance to build credit; pay in full and skip the interest.

- Closing old cards can raise utilization and shorten history — often keep them open.

- Income, job, and age are not in your credit score; you also have many scores, not one.

- Paying a collection doesn’t auto-delete it, and accurate items can’t be disputed away.

Want the facts on your own credit?

A free 15-minute review cuts through the myths and shows what’s actually on your report and affecting your score — no jargon, no sales pitch.

Free · about 15 minutes · no credit card · no obligation.

Sources: Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) — how credit scores work and common misconceptions; FICO and VantageScore scoring guidance. General education, not financial advice.