Renting after a denial

Denied an Apartment for Income? Here’s What That Means.

You can have decent credit and still be turned down over income — the ratio, the proof, or the debt behind it. Here’s how landlords read income, and how to put forward an application they can say yes to.

Quick answer

Most landlords want to see monthly income of about three times the rent, documented and verifiable. A denial “for income” usually means your income falls below that ratio, couldn’t be verified, or your existing debts take too much of it — not that you did anything wrong.

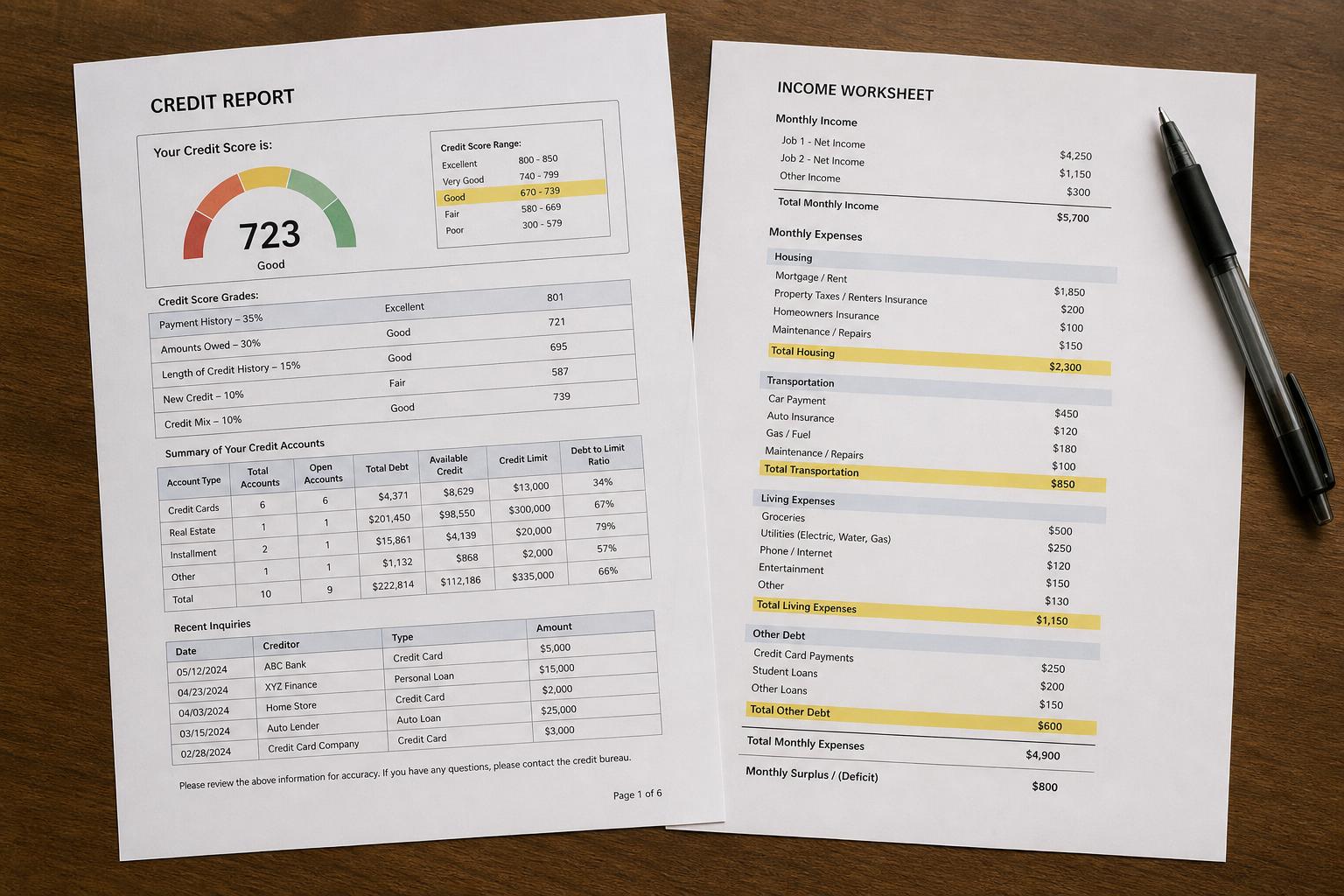

Income and credit overlap: collections, high balances, or unpaid debts on your report can be read as income risk even when your paycheck is fine. Knowing what’s on your report and documenting your income clearly are the two things most within your control.

What does it mean to be “denied for income”?

When a landlord cites income, they’re usually pointing at one of three things: your income is below their required ratio to the rent, it couldn’t be verified from the documents you provided, or your existing monthly debts leave too little of it for the rent. Many leasing offices run an automated check, so a borderline number can trigger a “no” without much explanation.

The good news is that income is one of the most fixable parts of an application — not by earning more overnight, but by documenting what you have clearly, adding a co-signer or roommate, or applying to a unit whose rent fits the ratio. Unlike a years-old credit mark, an income denial is often about presentation.

How much income do you need to rent an apartment?

The most common rule of thumb is gross monthly income of about three times the rent — so a $1,500 apartment often calls for roughly $4,500 a month before taxes. Some landlords use 2.5x, some require more in expensive markets, and some look at your income after debts rather than a flat multiple. There is no single legal standard; it varies by landlord and location.

Because the threshold isn’t universal, it’s worth asking a leasing office their exact requirement before you apply and pay a fee. If you’re close, the gap can often be closed with a co-signer, a larger deposit, or a slightly lower-rent unit.

Can you be denied for income even with good credit?

Yes. Credit and income are scored separately. You can have a clean report and still fall short of the income ratio, or have income that’s hard to verify — a brand-new job, self-employment, or cash work. A landlord weighing risk may approve a thin-credit applicant with strong, documented income and decline a good-credit applicant whose income can’t be confirmed.

That’s why a denial isn’t always about the obvious thing. Asking the landlord which factor drove the decision tells you where to focus — and sometimes the answer points back to your report after all.

How do income and credit interact on a rental application?

Landlords often read your credit report partly as an income-risk signal. Large balances, collections, or a high share of income already committed to debt can make even a solid paycheck look stretched. So “income” and “credit” aren’t always cleanly separate — what’s on your report can shape how your income is judged.

Debt-to-income, informally

Even when a landlord doesn’t calculate a formal debt-to-income ratio, monthly obligations on your report — car loans, cards, student loans — reduce the income they count as available for rent. Lowering what’s reported as owed, or correcting balances that are wrong, can change that picture.

Collections as a red flag

A utility or prior-rent collection can signal “didn’t pay a recurring bill,” which weighs against you regardless of income. If a collection is inaccurate or doesn’t belong to you, you have the right to dispute it under the Fair Credit Reporting Act (FCRA).

What counts as income to a landlord?

More than just a paycheck. Most landlords will consider documented, stable income from many sources:

- Wages and salary (pay stubs, an offer letter)

- Self-employment and gig income (tax returns, bank deposits, 1099s)

- Social Security, SSI, or SSDI

- Pension or retirement income

- Child support or alimony you receive

- Housing vouchers or assistance, where applicable

In a number of states and cities, “source of income” is a protected category — meaning a landlord can’t reject you simply because your income comes from a voucher or benefits. These protections vary by location; the U.S. Department of Housing and Urban Development (HUD) and your state or city fair-housing office can tell you what applies where you live.

How do you prove income with a new job or nontraditional pay?

When you can’t hand over three months of pay stubs, build the case another way:

- New job: an offer letter on company letterhead stating salary and start date, plus your first stub once you have it.

- Self-employed or gig: the last one to two years of tax returns and recent bank statements showing consistent deposits.

- Cash or tips: bank deposit records and, if possible, a letter from your employer.

The goal is to show the income is reliable, not just present. A short cover note explaining your situation, attached to clean documentation, goes a long way with a flexible landlord.

What if your income is below the ratio?

You still have moves. A co-signer or guarantor with sufficient income can satisfy the requirement. A roommate changes the household income the landlord counts. A larger deposit or a few months’ rent up front can offset the perceived risk. And applying to a unit whose rent actually fits the ratio is sometimes the simplest fix.

Before assuming you can’t qualify anywhere, confirm what each landlord actually requires — and make sure nothing inaccurate on your report is dragging down how your income is read.

Self-employed or gig income: how do you document it?

Self-employment is the classic “denied for income” trap, because the money is real but harder to verify. Lead with tax returns (the year-over-year picture), back them with bank statements showing steady deposits, and add a profit-and-loss summary if your income swings month to month. If you work through platforms, their annual earnings statements help.

Presenting an average monthly figure across a year — rather than a single light month — gives a landlord a fair read. Consistency is what reassures them.

Can a landlord deny you based on where your income comes from?

It depends on where you live. The federal Fair Housing Act prohibits discrimination based on protected classes like race, disability, and family status, but it does not nationally cover “source of income.” However, many states, counties, and cities do protect source of income — meaning a landlord there can’t refuse you solely because your income includes a voucher, Social Security, or other benefits.

If you suspect a denial was really about the source of lawful income in a place that protects it, you can contact HUD or your local fair-housing agency. This article is general education, not legal advice — the rules genuinely vary by location, so verify what applies to you.

How to strengthen an income-based application

An income denial is one of the most recoverable. Give the landlord clean, verifiable proof and a way to say yes.

Do

Don’t

Watch out for these income-verification scams

Applicants under pressure are targets. The Federal Trade Commission (FTC) warns about schemes that prey on people who’ve been turned down.

Red flags before you pay anyone

The bottom line on income denials

Being turned down for income usually means a ratio, a verification gap, or debt — all more workable than they feel in the moment. Document your income clearly, close the gap with a co-signer or a better-fit unit, and make sure nothing inaccurate on your credit report is quietly counting against you.

Key takeaways

Before you reapply or pay another application fee, know what’s actually being reported. A free 15-minute review shows what may be hurting your application — and what to address first. See the free rental credit review →

Make sure it’s really your income — not your report

A free 15-minute review shows what’s on your credit report behind a rental denial — including debts or collections that may be read as income risk — and a realistic next step.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.