The honest answer

What Happens If You Ignore Medical Debt? The Honest Answer

Ignoring a medical bill feels easier than facing it — but it doesn’t make the debt disappear, and it can quietly narrow your options. Here’s what really happens, and why blindly paying is just as risky as ignoring.

Quick answer

Ignoring medical debt doesn’t make it go away. It can be sent to collections, may appear on your credit report (subject to recent medical-collection rules), and in some cases the creditor or collector can sue — potentially leading to a judgment and, in some states, wage garnishment.

But panic-paying a bill you haven’t verified is also a mistake, because medical bills are so often wrong. The better path is neither ignore nor blindly pay: verify, dispute errors, and negotiate.

Does medical debt go away if you ignore it?

No. An unpaid medical bill doesn’t expire just because you stop opening the envelopes. Left alone, it typically moves through a predictable sequence: reminders from the provider, then assignment or sale to a collection agency, then collection activity — and, in some cases, a lawsuit. Ignoring it mostly means losing control of when and how those steps happen, and surrendering the leverage you’d have by engaging early.

First, the bill goes to collections

If a medical bill stays unpaid, the provider often turns it over to a debt collector. At that point a third party is involved, and the FDCPA governs how they can contact you. A collection account is also the stage where your credit report can come into play — though, importantly, medical collections now follow special rules (next section). Once it’s with a collector, negotiating tends to be harder than it would have been with the original provider.

Will ignored medical debt show up on your credit report?

It might — but medical collections are treated differently than they used to be. The national credit bureaus made voluntary changes: paid medical collections are removed, there’s a waiting period (about a year) before an unpaid medical collection can appear, and medical collections under a certain threshold (around $500) are no longer reported. A broader CFPB rule that would have removed medical debt from credit reports was finalized in early 2025 but later vacated, so it’s not currently in effect. These rules have shifted and can vary — so whether an ignored bill hits your report depends on the amount, how long it’s been, and whether it’s been paid. Verify your own report rather than assuming.

Can you be sued for unpaid medical debt?

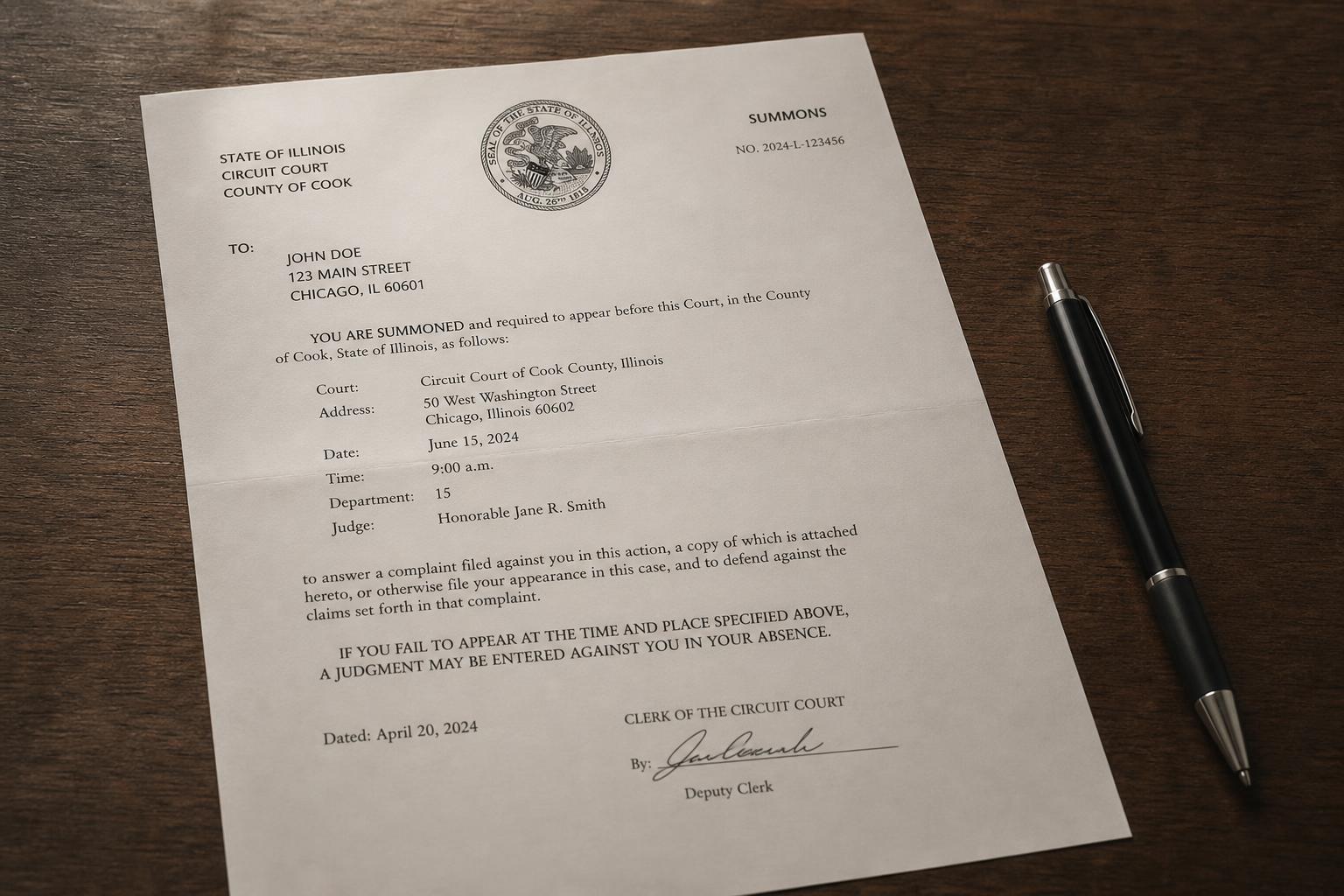

Yes. A provider or a collector that bought the debt can file a lawsuit, and if you don’t respond, they can win a default judgment. A judgment can open the door to consequences that vary by state, potentially including wage garnishment or bank-account levies. This is the most serious reason not to simply ignore medical debt: the lawsuit, not the bill itself, is where ignoring can really hurt. (The statute of limitations limits how long they can sue — but you generally have to show up and raise it.)

Never ignore a summons

If you’re served with a lawsuit, respond by the deadline even if the debt is old or disputed. Ignoring a summons is how a beatable case becomes a judgment.

What does ignoring it do to your options over time?

Mostly, it shrinks them. Early on, you can itemize the bill, catch errors, apply for financial assistance, and set up an interest-free plan with the provider. After it goes to collections — and especially after a judgment — those friendly options narrow, and you’re negotiating from a weaker spot. Time generally works against you here, which is why “deal with it later” tends to cost more than dealing with it now.

But don’t panic-pay either: why verifying first matters

The opposite mistake is just as common: paying a medical bill immediately, in full, to make it go away. Medical billing errors are widespread — duplicate charges, services never rendered, insurance not applied, balances that should have been covered. If you pay before verifying, you may be paying for someone’s mistake. So the goal isn’t “pay fast” any more than it’s “ignore” — it’s “verify, then decide.”

The middle path: verify, dispute, negotiate

Between ignoring and panic-paying is the approach that actually protects you:

- Verify the bill is accurate and yours — get an itemized bill and check it against your insurance EOB.

- Dispute errors with the provider, collector, or credit bureaus, as your rights allow.

- Negotiate — ask about charity care, discounts, and interest-free payment plans.

This keeps you in control, ensures you only pay what you truly owe, and often resolves the debt on far better terms than either extreme. A free 15-minute review can help you see what’s reporting and what may be disputable.

What if you genuinely can’t pay?

If the bill is real and you simply can’t afford it, you still have avenues besides ignoring it. Apply for the hospital’s financial assistance or charity care (often required at nonprofit hospitals and income-based). Ask for an interest-free payment plan sized to what you can actually pay. Look into local or condition-specific assistance programs. And if you’re facing lawsuits or overwhelming debt, a legal-aid office or nonprofit credit counselor can help you understand your options. Engaging, even to say “I can’t pay this in full,” beats silence.

How long does medical debt stay a problem?

Two separate clocks again: the statute of limitations (state-set, often a few years) limits how long you can be sued, while credit reporting follows its own timeline — and medical collections may come off sooner under the bureaus’ rules, or not appear at all if paid or small. A debt can stop being a credit-report problem while still being collectible, or vice versa. Knowing where a specific debt sits on each clock tells you how urgent it really is.

The right way to handle medical debt you’ve been avoiding

Re-engaging is the move — on your terms, with the facts in hand.

Do

Don’t

Red flags while you sort it out

People with avoided debt are targets for pressure and scams. Be wary of:

Red flags

The bottom line on ignoring medical debt

Ignoring medical debt doesn’t resolve it — it just moves it toward collections and, sometimes, a courtroom, while your best options quietly expire. But the answer isn’t to panic-pay either, because the bill may well be wrong. Verify it, dispute what’s inaccurate, and negotiate what’s real. That middle path protects both your wallet and your credit.

Key takeaways

Before you pay or settle a medical bill, confirm what’s actually reporting. A free 15-minute review shows what may be inaccurate, outdated, or disputable — before you act. See the free medical-debt review →

See where your medical debt really stands

A free 15-minute review shows what’s on your credit report and what medical items may be inaccurate, already ineligible to report, or disputable — so you can act on facts instead of fear.

Find Out Why I Was DeniedNo credit card · phone optional · no obligation.